Market Update: Data Dependent

US equity indexes were mixed on the week: S&P500 +0.95%, NASDAQ +1.74%, and DJIA -0.11%. Both market participants and the Fed are trying to finely calibrate the timing first Fed rate cut, making both excessively data-dependent. While the CPI and PPI for January surprised to the upside, PCE prices for January, released this week, came in on expectations. This result was a relief and lifted equity indexes and weighed on bond yields. It seems that the last part of the journey back to 2% inflation could be complicated, and the Fed is emphasizing data collection as opposed to having confidence in its economic projections.

The US 2 year yield fell 16bps this week to 4.5292% and the 10 year yield fell 7bs to 4.1798%. Nvidia closed with a market cap above USD 2 trillion for the first time, and is only the third US company to do so after Apple and Microsoft. Bitcoin (XBTUSD) continued its rally, crossing 60,000 this week (Friday afternoon it stood at 62,621), fueled by inflows to spot-Bitcoin ETFs. After Friday market close, the United States was affirmed at AA+ by Fitch.

US Economic Data and Fed Pricing:

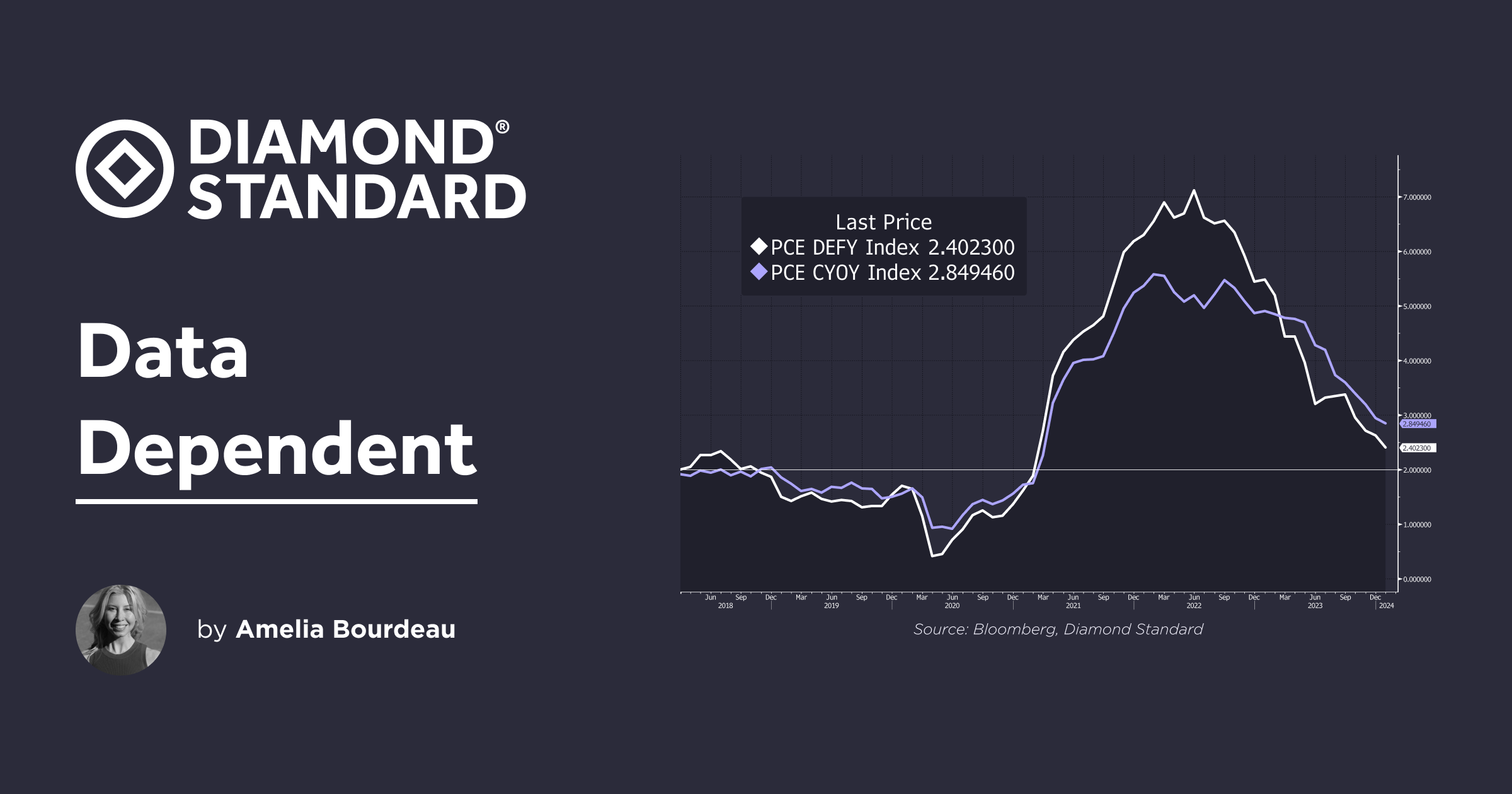

After the upside surprise to the US January CPI readings, January PCE price results were highly anticipated by market participants. The headline and core PCE deflators were both in line with consensus expectations. Headline PCE deflator fell to 2.4% y/y from 2.6% in December. Core PCE deflator, the Fed's preferred measure of inflation, ticked down to 2.8% y/y from 2.9% in December.

The eye-catching upward surprise in the data release was the strong 1.0% m/m jump in personal income, which is the largest gain since the start of 2021. January, however, does bring one-off adjustments at the start of the year for the cost-of-living adjustment to Social Security and to personal tax payments which can impact the number.

Fed funds futures are pricing in approximately 90 basis points of rate cuts for the year, which is a bit less than four 25bp rate cuts. Pricing is converging toward the Fed's forecast, which expects three 25bp rate cuts for 2024. No rate cut is expected at the March FOMC meeting. Market participants have reduced their expectations for a 25bp rate cut in May to a 23% probability. Consensus is forming around an initial 25bp rate cut in June with a 57% probability priced.

Chart: US PCE and Core PCE Prices Y/Y% and Fed Target

Precious Metals:

We continue to favor an allocation to precious metals including the diamond commodity for diversification and safe-haven purposes. Financial markets could be impacted by several potential sources of volatility this year including geopolitical tensions, global elections, and now both growth and inflation shocks. These potential financial market disruptors should create demand for precious metals as a hedge. In the second half of the year, Fed easing should support gold and silver. A strong to steady US consumer is a positive for the diamond market.

Diamond Industry

DIAMINDX is currently at USD 4,330, up 3.3% from its low the first week of November 2023. The natural diamond industry is emerging from the supply overhang which hindered it in 2023 after two years of record consumer diamond demand. The industry is starting 2024 with a sense of equilibrium. The US economy, the world's largest consumer of diamonds, remains strong. There is increasing push-back on the lab grown diamond industry regarding questionable descriptions of the diamond product and claims of sustainability. Independent diamond analysts believe that demand for lab grown diamonds is leveling off.

Cormac Kinney, Founder and CEO of Diamond Standard, announced that Mark Cutifani, former Chair of DeBeers Group and CEO of Anglo American, has joined the Diamond Standard board of advisors. "Mark's global perspective and experience will help us to apply our technology to unlock other natural resources as investable assets." said Kinney. (See the announcement here and in the FT here).

Rapaport News reports that New York's diamond dealers are upbeat as a result of the tight natural diamond supply. Holiday sales were steady and while restocking is slow, "New York dealers are reporting firm pricing on the local and Indian markets. This is mostly because there aren’t enough diamonds coming out of India; the inventory surplus that froze the market in 2023 has abated," says Rapaport News.

Turning to lab-grown diamonds, Business Insider released an article in which it spoke to industry analysts who largely agree that lab-grown diamonds have become "mainstream" and that their prices will continue to fall due to a supply glut. Independent diamond analyst Paul Zimnisky gave his thoughts to Business Insider, saying that he "foresees jewelers scaling back their business in lab-grown diamonds while ramping up their focus on natural diamonds over the next year. In fact, most jewelers aren't even bothering to stock lab-grown diamonds in inventory, and are only purchasing them on consignment."

Lightbox, DeBeers Group's lab-grown diamond business, lowered prices for select goods in Q4 2023. According to National Jeweler, in Q4, "Lightbox dropped the price of its standard lab-grown diamonds (G-J color and VS clarity) from $800 per carat to $600 per carat.. its 'Finest' range was reduced to $1,000 per carat, down from $1,500 per carat." Lightbox says that "consumers can anticipate new prices from the company in the coming months." These new prices will most likely be lower in keeping with the industry trend. Currently, Lightbox has put certain items on sale on its website, offering lab-grown diamond 1ct. tw. round brilliant studs for $540 and 1.5ct tw studs for $720 (about $480 per ct). Perhaps this is a new, lower price test by Lightbox.

Diamond industry events this week include the Hong Kong International Diamond, Gem, and Pearl Show and the Hong Kong International Jewelry Show, both of which are underway and are among the largest jewelry trade shows in the world. China's economy has been sluggish post-Covid, so these trade shows could signal what is ahead on the demand front in 2024 for the region.

Gold and Silver

Gold rallied on the week, rising 2.4% to USD 2,083 as the USD and US yields backed off since US economic data did not surprise to the upside. Similarly, silver was supported and rose 0.9% on the week to USD 23.15, breaking above USD 23.00 resistance. Both gold and silver are largely trading off of US economic data and shifting Fed rate cut pricing.

The World Gold Council ("WGC") has released its January 2024 gold ETF flows report. Gold prices were weighed on as market participants scaled back their Fed easing expectations. Global physically backed gold ETFs had USD 2.8bn of outflows in January, led by North America. With the rally in US equity indexes, the focus on AI stocks, and the launch of Bitcoin ETFs, US investors leaned into risk-seeking, which hindered gold in January. The global USD 2.8bn outflow "was equivalent to a 51t reduction in global holdings, to 3,175t by the end of January. Meanwhile, total assets under management (AUM) fell to US$210bn, a 2% decline due to outflows in the month."

Chart: Gold ETF Flows

USD

USD (DXY Index) was down a slight 0.1% on the week to 103.88, having moved sub-104.00. Support comes in at 103.75 (200 day movg).

USD has been trading in a narrow 103.45-104.90 since the start of February. With all of the US economic data surprises and the shift higher in US yields across the curve year-to-date, one would expect the USD to have been on the move more - ie reacting strongly. However, FX volatility is low currently for the major currencies. Market participants have been wary to push EURUSD below 1.0700, USDJPY currently above 150.00 is in intervention territory so traders will not touch it at those levels, and GBPUSD has been in a tight 1.2525-1.2750 range since the start of the year. Market participants are unsure of which G10 central bank will cut rates first, which plays into the lack of position-taking.

A combination of economic outperformance, US equity market exceptionalism, and discussions on higher structural productivity, continue to support the USD.

Chart: Select FX Volatility - 3 month ATM Volatility

Ahead:

The main data release next week is US Payrolls for January. The consensus estimate expects a 200k gain and for the unemployment rate to remain at 3.7%. ISM Services for February will also be of interest.

Fed Chairman Powell will give his Semiannual Monetary Policy testimony before the Senate Banking Committee on March 7th.

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.