Market Update: Bumps in the Road

US equity indexes were down on the week: S&P 500 -2.1%, NASDAQ -2.7% and DJIA -1.7%.

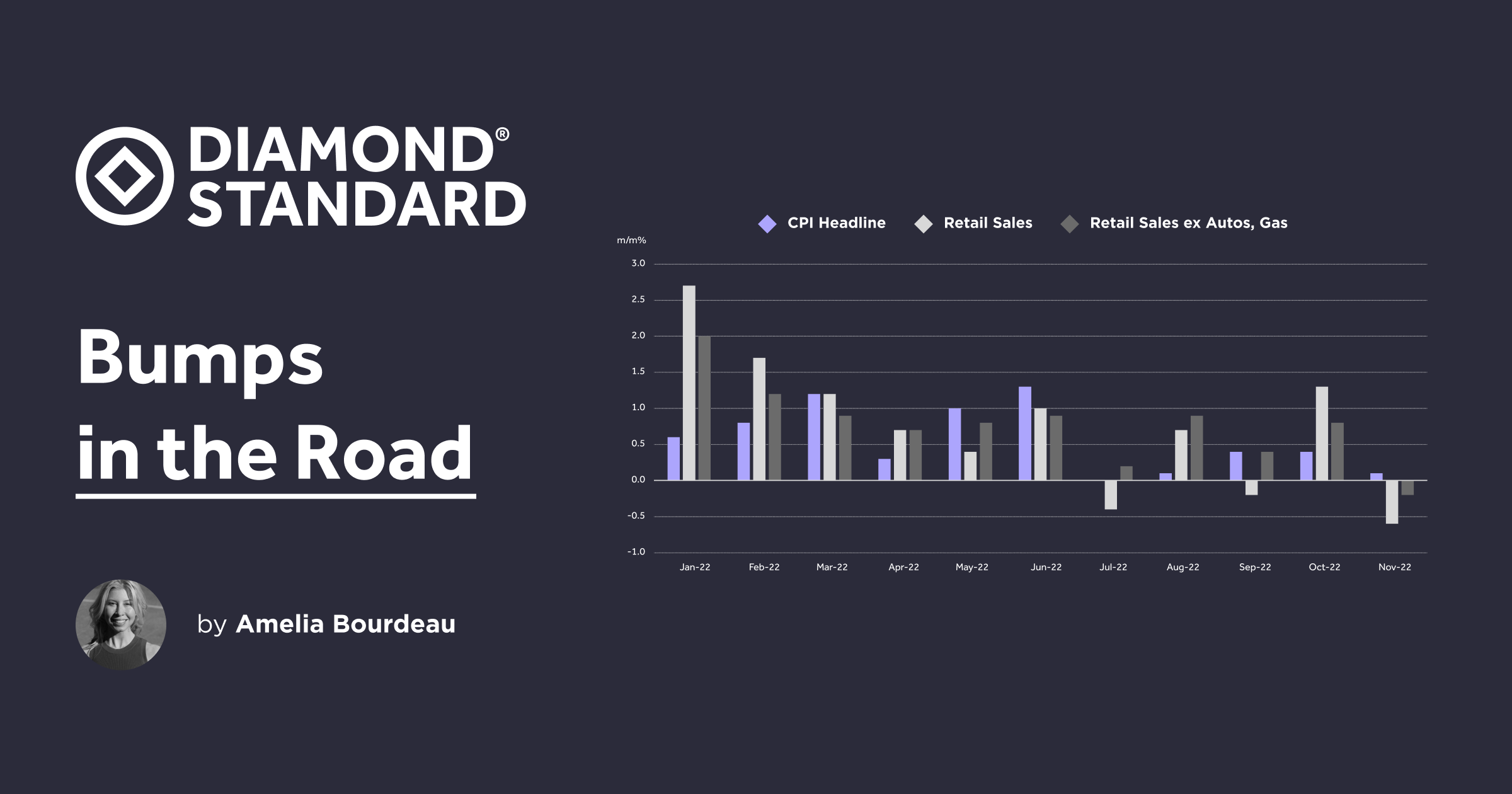

The Fed delivered a 50bps rate hike at its December meeting as expected, which is a slowing of the pace of rate hikes from clips of 75bps. However, market participants focused on Powell's more hawkish comments at the press conference (see below). Both US headline and core CPI surprised to the downside in November - a positive development. Headline CPI rose 0.1% m/m in November 2022, after increasing 0.4% m/m in October. Headline CPI increased 7.1% y/y in November, slowing from 7.7% y/y in October. The November read was the smallest 12-month increase since December 2021. Core CPI increased 0.2% m/m to come in at 6.0% y/y down from 6.5% y/y in October. On a less positive note, US retail sales fell 0.6% m/m in November for its largest drop in a year - a negative development.

Overall, worries about the Fed tightening into a slowing US growth environment weighed on US equity indexes. It is apparent that the next shocks to markets will likely be on the growth front as the full extent of the Fed rate hikes have not yet been felt and there is concern that the Fed can not "soft land" the economy. The road into 2023 is getting bumpy.

Turning to the FOMC meeting, as expected, the committee hiked the Fed Funds rate by 50bps to the target range of 4-1/4 to 4-1/2 percent. In the median forecasts, the Committee displayed a hawkish bent in its Summary of Economic Projections ("SEP"), expecting the Fed Funds rate to end-2023 and 2024 at 5.1% and 4.1% respectively (4.6% and 3.9% were the forecasts in September), only coming back to 2.5% in the "longer run." Core PCE inflation forecasts were revised up as well to 3.5% in 2023 and 2.5% in 2024, compared to 3.1% and 2.3% in September. While the Fed may be nearing the end of its tightening cycle, the start of an easing cycle is not in the committee members near-term view.

Key Powell quotes from the press conference:

On inflation expectations: "Despite elevated inflation, longer-term inflation expectations appear to remain well anchored...But that is not grounds for complacency; the longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched."

On the inflation fight: "We are taking forceful steps to moderate demand so that it comes into better alignment with supply... Reducing inflation is likely to require a sustained period of below-trend growth and some softening of labor market conditions."

On the possibility of rate cuts: "I guess I would say it this way: I wouldn't see us considering rate cuts until the Committee is confident that inflation is moving down to 2 percent in a sustained way. So that's the...Test I would articulate. And you're correct. There are not rate cuts in the SEP for 2023."

Full press conference transcript here.

Chart: US Headline CPI, Retail Sales and Retail Sales ex Autos & Gas (m/m%). While the moderation in CPI was welcome, the moderation in retail sales was not. Source: Bloomberg, DS

USD flat to down

USD, DXY Index, fell 0.10% on the week. The DXY Index ranged 105.23-103.45, ending the week at 104.60 area.

The ECB hiked its refi rate 50bps to 2.50%, as expected. President Lagarde was hawkish, saying that the rise in the ECB's inflation forecasts meant that the ECB had more work to do to meet their inflation goal. Lagarde also noted that the ECB saw the terminal rate as higher than the market was pricing, which was 2.85%. The combination of a USD on its backfoot post the weaker than expected US CPI and a hawkish Lagarde pushed EURUSD above 1.0700 during the week. However, the single currency finished the week at 1.0586 - a gain of 0.47% vs USD.

The BoE hiked its policy rate by 50bps to 3.50%, as expected. However, there were three dissenters to that decision - two in a dovish direction (they wanted no change to the policy rate ) and one dissent in a hawkish direction (wanted a 75bp rate hike).This highlights the uncertainty in the economic outlook. The BoE said it will start selling debt across short, medium, and long-maturity bonds staring January 9 as part of its quantitative-tightening program. Sterling was the worst performer during the week vs USD, falling nearly 1.0% to 1.2142. The UK is facing a cost of living crisis and the possibility of strike action across various UK industries. These factors should keep GBP on its backfoot ahead especially vs. EUR, where the ECB is seen to be more hawkish than the BoE.

JPY was one of the stronger performers vs USD during the week as USDJPY continued to track the US 10 year yield lower.

Chart: S&P 500 (inverted), US 10 year yield, DXY Index. Source: Bloomberg, DS

The Diamond Commodity

DIAMINDX fell 0.2%, gold fell 0.24%, and silver fell 1.0% on the week.

Gold was boosted on Tuesday with the weaker US CPI print for November. As the USD weakened on the result, gold shot up above USD 1,820. However, hawkish forecasts from the Fed's SEP (discussed above) ended up tempering gold and it finished the week at USD 1,793. Silver followed a similar pattern reaching USD 23.94 mid week only to back off to USD 23.22 by the week's end.

The movements in USD and US yields are impacting gold and silver prices. However, as DIAMINDX is uncorrelated, those movements do not impact its price, which has been moving lower. Holiday jewelry sales are made relatively last minute and so far US jewelers are seeing demand below the outsized 2021 gain but on par or slightly ahead of 2019 - a pre-pandemic year.

Chart: DIAMINDX seasonality - ave of past 5 years shows gains in the index in December, January and February. Source: Bloomberg, DS

Diamond News:

Petra Diamond's latest tender results were mixed and showed signs of rough diamond prices stabilizing. Like-for-like prices increased 2.2% for December compared to the previous sale, which took place in October and November.

The results of Tender 3 bring FY 2023 YTD revenue from rough diamond sales to USD 206.4 million, with no Exceptional Stone sales, compared to USD 264.7 million in the first three tenders of FY 2022, which included a USD 77.9 million contribution from Exceptional Stones. The lower volume sold in Tender 3 relative to the equivalent tender in FY 2022 was largely driven by the earlier cut-off date for the current cycle.

Richard Duffy, CEO of Petra stated: "Prices in the 2ct to 10ct size ranges saw an upward movement in contrast to the recent negative trends, partly ascribed to improving expectations for the current festive season and potentially reflecting signals from the Chinese authorities with respect to an easing of lockdown restrictions. Prices in smaller size ranges saw improved pricing which more than offset softer pricing in the 0.75ct to 2ct ranges."

A rare pink diamond was pulled from Christies NYC December 6 magnificent jewels auction. National Jeweler covers the reason why in this intriguing story.

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.