Market Update: Chopping Around

US equity indexes were up on the week: S&P 500 +0.8%, NASDAQ +0.3%, and DJIA +1.2%. They continue to shake off March's banking sector turmoil. Volatility is moderating: the VIX fell further to a 15 month low of 17.07 and the BoA MOVE Index, which measures implied volatility of one month treasury options, moved lower to 118.8 vs 139 last Friday, though it is still elevated. The KBW regional bank index fell 1.5%, but the wider KBW bank index rose 3.2%. March retail sales were disappointing, while CPI eased at the headline but ticked stubbornly up for the core read (more below). As the Fed is data dependent, markets remain choppy - reacting to nearly each individual US economic data point. These are tactical trading conditions.

On the US Data Front:

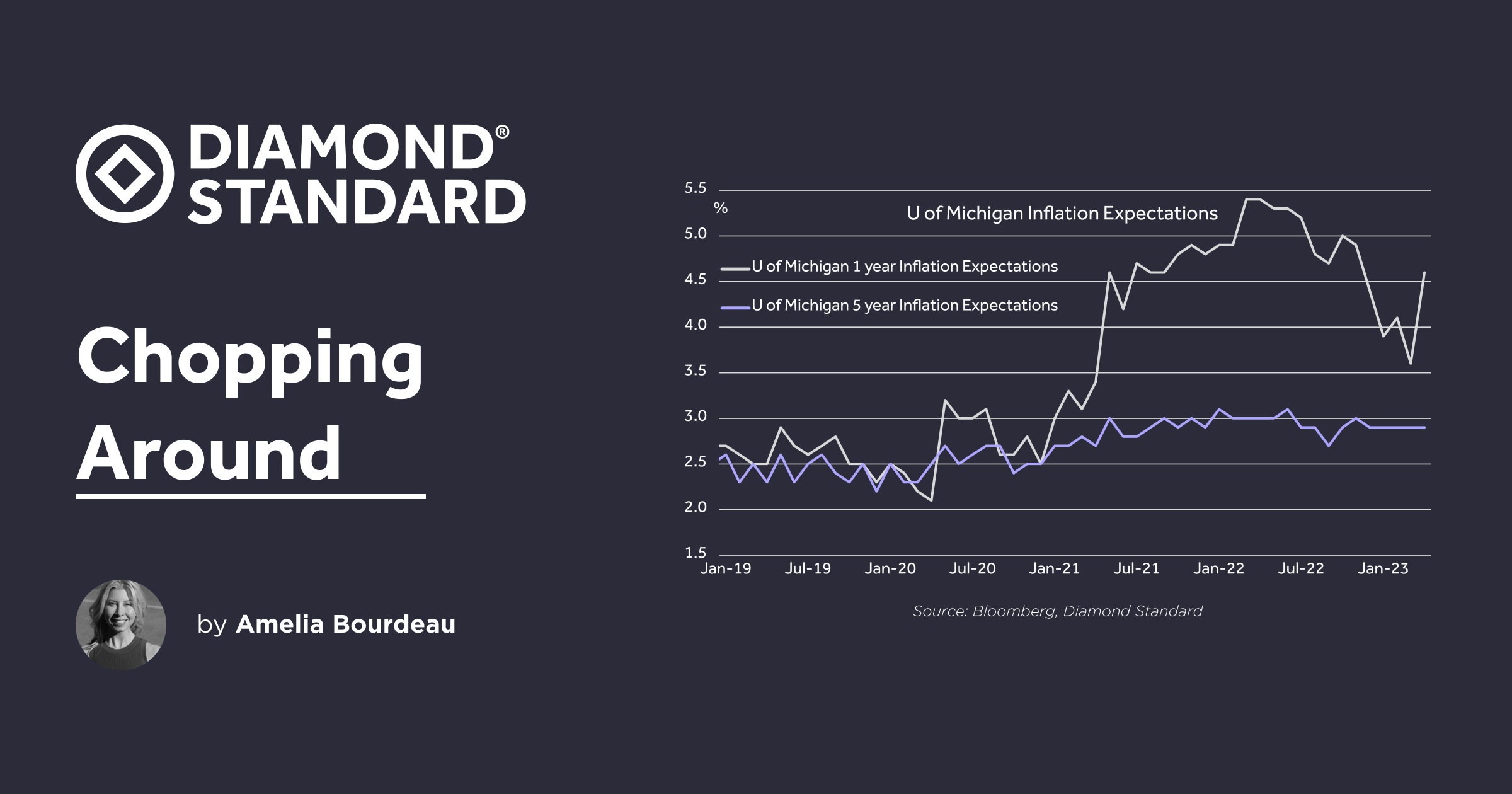

University of Michigan sentiment was stronger than expected for April coming in at 63.5 up from 62.0 in March and vs expectations of 62.1. What was surprising was 1 year inflation expectations, which jumped from 3.6% to 4.6% (chart below). This is the largest gain in about 2 years. Longer term inflation expectations, 5-10 years, remained unchanged at 2.9% - this is the measure the Fed focuses on.

US retail sales for March fell across the board. Headline retail sales fell 1.0% m/m. Core retail sales fell -0.3% m/m vs expectations of -0.6%m/m and the retail control group (GDP input to PCE) fell 0.3% m/m vs expectations of -0.5%.

March CPI rose 0.1% m/m to come in at 5.0% y/y down from 6.0% y/y for the previous read. Energy prices had their second monthly decline. However, relevant for the April read ahead, gasoline prices are up about 15 cents per gallon since March 31st. Core CPI rose 0.4% to come in at 5.6% y/y - an uptick from February's read of 5.5% y/y.

Released a day after CPI, PPI (producer price index) for March fell a more than expected 0.5% m/m. While not a Tier 1 economic indicator, the market nevertheless reacted. The lower price reading weighed on the USD and bond yields on Thursday.

Chart: University of Michigan Inflation Expectations - a jump in 1 year expectations

__Fed-Speak: __

Comments from Fed officials were back and forth this week. Fed Governor Waller (voter) said he favored more monetary policy tightening: “Because financial conditions have not significantly tightened, the labor market continues to be strong and quite tight, and inflation is far above target, so monetary policy needs to be tightened further." Chicago Fed President Goolsbee (voter) seemed to favor a pause: "Let’s just be mindful that we’ve raised a lot, it takes time for that to work its way through the system." Though he said that he needs to see more data before the Fed's next meeting.

Fed Pricing:

Fed funds futures are pricing about an 80% chance of a 25bp rate hike at the May FOMC. A small probability of another 25bp tightening is being priced in for June (at the time of writing). 79bps of rate cuts are priced in from July through January 2024.

The table below shows, in more recent Fed history, the "turn-around time" in months from the terminal fed funds rate to the first rate cut. If a rate cut is delivered in July or September, either 2 or 4 months from the terminal fed funds rate, that would be a quick turn-around relative to the other tightening periods shown.

Table: Fed rate hiking cycles and "turn-around" time (source: DS, Bloomberg, FRED)

Precious Metals:

DIAMINDX fell 0.2% on the week to USD 5,270. The diamond industry received some positive news on demand in China:

LVMH, the world's largest luxury goods company, reported a 17% y/y rise in Q1 sales - more than double analysts' expectations. This was mainly attributed to a sharp China rebound after its Covid-19 lockdowns eased (i.e. the China reopening theme). LVMH noted that "the United States, a market which continues to grow, had a steady performance." Asia ex Japan accounted for 36% of the Q1 revenue growth and the US accounted for 23%. The US and China are the world's two largest consumer markets for diamonds, so it is positive that there is demand in both regions for luxury goods. LVMH's watches and jewelry sales rose 11% y/y. In jewelry, LVMH noted in its press release that "Tiffany & Co. had an excellent start to the year as preparations were made for the upcoming reopening of the Landmark (5th Avenue store) in New York." Bulgari also showed strong growth especially in one of its high jewelry collections.

Despite caution among retailers on the outlook for the US consumer, __the LVMH results are a bright spot, showing resiliency in consumer spending in the high end segment of retail markets. The results also highlight the tailwind for the diamond and jewelry industry that can come from the long-awaited China reopening. __

On a side note, according to Bloomberg News, LVMH broke into the world's top 10 companies by market value briefly this week, as its Q1 results rallied its share price. That, along with a gain in the EURUSD, lifted LVMH’s market capitalization to USD 486 billion.

De Beers Group released the results of its Cycle 3 rough diamond tender. Rough sales came in at USD 540 million, up 8.6% from Cycle 2 and down 4.6% y/y. CEO Al Cook said: “We have continued to see good demand for our rough diamonds over the third sales cycle of the year as we move into the second quarter of 2023. Sales were in line with expectations and we continue to see some encouraging positive trends in consumer demand for diamond jewelry, not least in China where we’re beginning to see some signs of recovery in consumer confidence following the relaxation of travel restrictions.”

Gold Gold was basically flat on the week, ending at USD 2,005 but it had traded as high as USD 2,040 earlier in the week. Erasing a possible weekly gain for gold was the stronger than expected U of Mich 1 year inflation expectations read, which boosted the USD and US yields on Friday. Gold continues to be impacted by bond market volatility.

Silver Silver gained 1.7% on the week, breaking resistance at USD 25.00 to end at USD 25.38. This is silver's fifth consecutive weekly gain.

Chart: De Beers Group Rough Diamond Sales - gaining momentum in 2023

USD

The USD (DXY Index) was down 0.5% on the week. It broke downside support at 102.00 to end the week at 101.57. 100 is the next support - a level DXY has not traded at since April 2022. A further dip in US bond yields on the back of the weaker than expected PPI pushed USD lower - through 101.00 on Thursday, but USD rebounded on Friday. EURUSD, the DXY's largest component, broke topside 1.1000 resistance and finished the week there.

Chart: Movements in the DXY Index and EURUSD this week with relevant data releases noted

Ahead - select events:

US economic indicators next week are generally Tier 2 and include housing data.

Tuesday, April 18

- China Q1 GDP

- US Housing Starts (Mar)

- Canada CPI (Mar)

Wednesday, April 19

- ECB's Schnabel speaks

- UK CPI (Mar)

- NY Fed Pres Williams speaks

- Chicago Fed Pres Goolsbee speaks

Thursday, April 20

- US Existing Home Sales (Mar)

Sign Up for Market Commentary: Weekly insights on global markets and commodities from Diamond Standard by Amelia Bourdeau

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.