Week in Review: Confirmation

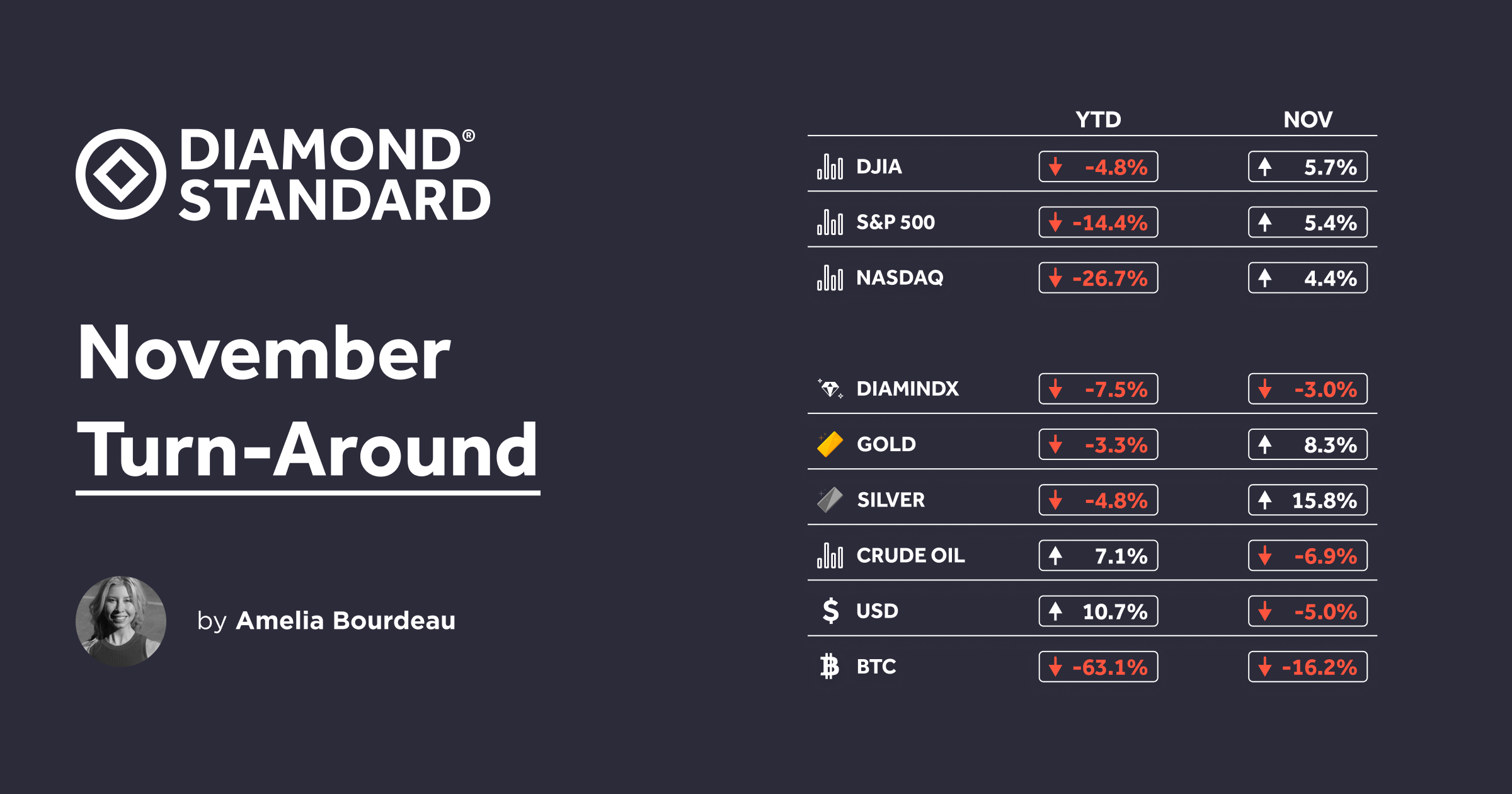

US equity indexes gained for the week: S&P 500 1.1%, NASDAQ 2.1% and DJIA 0.2% supported by Fed Chair Powell's remarks at the Brookings Institute (see below). Some asset classes (US equity indexes, gold, and silver) had big turn-arounds for the month of November and into the final stretch of the year (table) as market participants think there will be a backing off of aggressive Fed rate hikes. This sentiment weighed on US bond yields and the USD, while boosting equities. Bitcoin was negatively impacted by the fallout from the FTX situation.

Table: Performance YTD and November

Last week, the November FOMC minutes signaled that slowing the pace of rate hikes "would likely be soon appropriate." As a result, this week, market participants were looking for confirmation of this sentiment from Fed Chair Powell at his highly anticipated speech on inflation and the labor market at the Brookings Institute on November 30th.

Powell did confirm that a slowing in the pace of rate hikes was likely stating, "Monetary policy affects the economy and inflation with uncertain lags, and the full effects of our rapid tightening so far are yet to be felt. Thus, it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting." On the day, US equity indexes rallied and US bond yields fell, as did the USD. Watch Powell's speech here.

But the week was not over - on Friday US November payrolls were released. The jobs data came in stronger than expected, rising 263k vs the Bloomberg consensus expectation of 200k. The unemployment rate was unchanged at 3.7%. Importantly, wages rose 0.6% m/m, the largest monthly gain since January, and 5.1% y/y - likely not a result the Fed wants to see. These data continue to point to strength in the US labor market even as expectations of a recession in the future grow.

Chart: Whiplash - US 2 yr and 10 yr yields intraday over 3 days. The decline on Nov 30 is post Powell's speech and the spike on Friday post the US payrolls release (chart time 9:00am EST Friday)

In other US data of note this week, the US ISM Manufacturing index fell 1.2 percentage points to 49% in November - a figure below 50.0, indicating contraction in the manufacturing sector.

Turning back to Powell's Wednesday speech at Brookings, he included the chart below in his presentation - components of core PCE inflation and spoke about it in his remarks. He stated, "Core goods inflation has moved down from very high levels over the course of 2022, while housing services inflation has risen rapidly. Inflation in core services ex housing has fluctuated but shown no clear trend." Core services less housing is the largest of the three categories. On that category, Powell noted, "Thus, this may be the most important category for understanding the future evolution of core inflation. Because wages make up the largest cost in delivering these services, the labor market holds the key to understanding inflation in this category." As the November payroll data confirm, discussed above, wages (ie average hourly earnings) are still rising strongly.

Chart: Chart from Powell - Components of core PCE Inflation

USD - DXY breaks downside 105.00

USD (ie the DXY Index) continues to be driven by Fed-speak and the reaction of US yields. The DXY Index broke 105.00 downside support to end the week at 104.54. The next major support is 103.00-102.95 - around the March 2020 high. The USD had notable declines this week vs all G10 currencies except CAD. EURUSD, the DXY's largest component, closed the week at 105.35 - the single currency's highest level since June. USDJPY continues to track the US 10 yr treasury yield lower. USDJPY fell below the 200 day moving average on Friday, closing at 134.31. Meanwhile Sterling rallied topside through its 200 day moving average also on Friday, ending the week at 1.2280.

Chart: DXY Index (USD): Downside break of 105.00 - a significant support

The Diamond Commodity

DIAMINDX fell 0.5%, gold rose 2.4%, and silver rose 6.4% on the week.

DIAMINDX is seasonally weak in November, but on average over the past 5 years, has bounced back in December. Most holiday jewelry sales are made relatively last minute and December price action for DIAMINDX reflects this. The decline in USD, especially the downside break of 105.00 in the DXY Index has led to a strong rally in gold and silver. Gold traded above $1800 on Thursday closing the week at $1797.63. Since its low on September 26th, gold is up by $175.27. On Friday, the stronger than expected US payroll result saw gold immediately dip by 1.2% as USD strengthened in reaction, but gold recovered throughout the remainder of the NY trading session. Silver has gained $5.10 since its low on September 9 and ended the week at $23.14. Silver is up approximately 9.2% since Powell's speech on November 30. Similar to gold, silver fell 2.2% immediately on Friday's payroll results before retracing all of that loss. See table above for DIAMINDX, gold, and silver returns for the month of November.

Chart: Though still in negative territory for the year, gold and silver have begun to outperform DIAMINDX YTD. However, DIAMINDX is poised for a strong December due to seasonals.

Diamond News:

Rough-Polished reports that Alrosa CEO Sergey Ivanov Jr. will step down before his contract expires. Alrosa produces a quarter of all diamonds in the world.

Petra Diamonds said its Williamson mine in Tanzania Is likely to remain closed for longer than expected following the dam breach a month ago.

Ahead, DeBeers Sight 10 dates are December 5 - 9.

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.