Market Update: Friday Jitters

US equity indexes were up on the week: S&P 500 +1.4 %, NASDAQ +1.7%, and DJIA +1.2%. The VIX Index remains above the key level 20.0 at 21.7. The BoA MOVE Index, which measures implied volatility of one month treasury options, is elevated at 173.6. Rates volatility is much higher than equity volatility. The KBW regional bank index stabilized a bit, rising 0.6% on the week after falling 9.4% last week. The wider KBW bank index fell 0.5% after being down 14.5% last week.

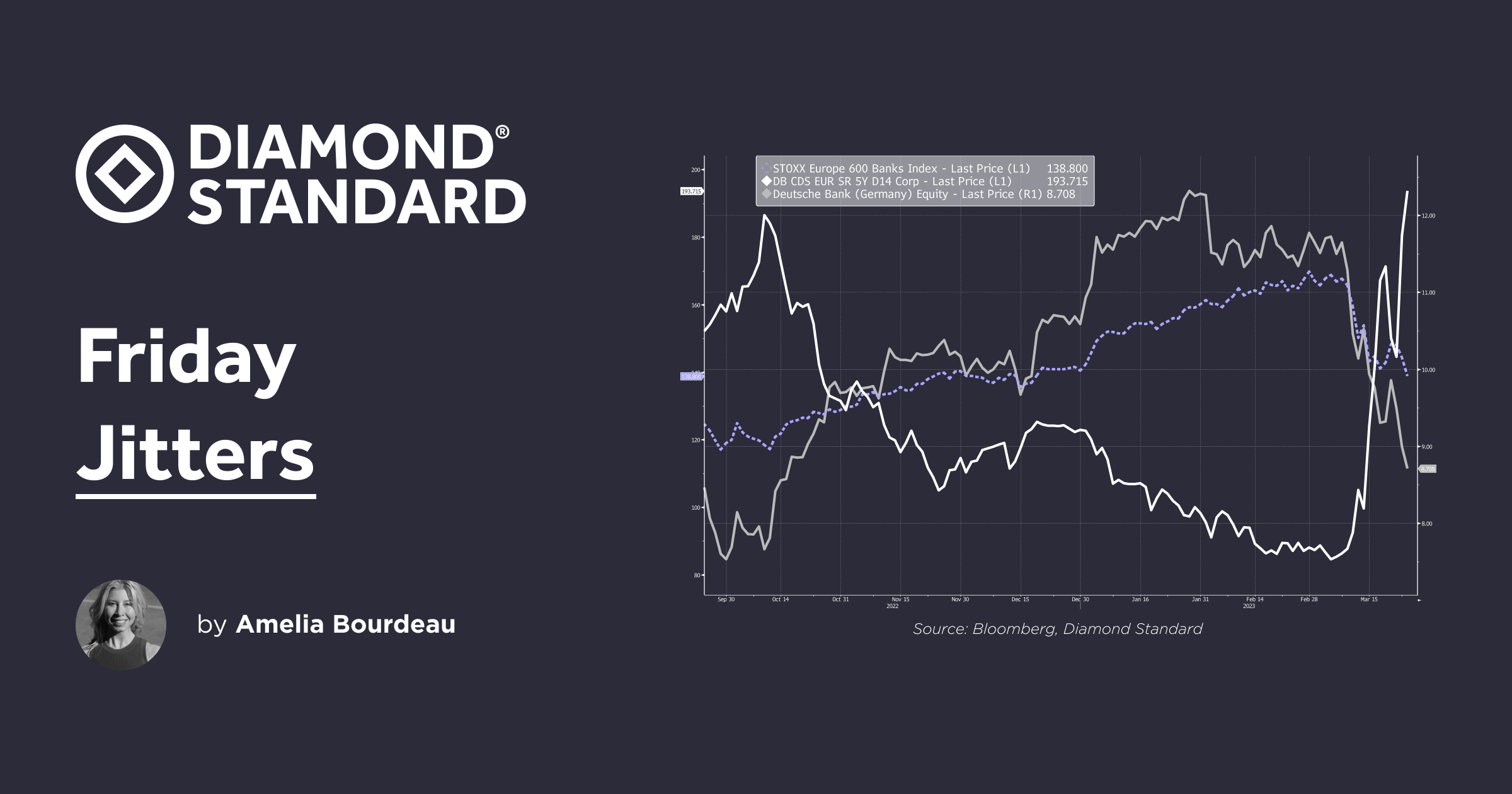

It was another jittery Friday in markets. Despite the takeover of Credit Suisse by UBS in a rescue deal last weekend, markets participants have remained concerned about European banking stocks post that event and the SVB failure in the US. On Friday, the market turned its attention to Deutsche Bank ("DB"). DB's CDS spiked on Friday. Its shares have been down for 3 consecutive weeks - falling 26% for March so far (chart below).

DB is one of 30 globally systemically important banks as identified by the Financial Stability Board, an international body that makes recommendations about the global financial system. Analysts struggled to pinpoint a reason for the concern about DB and subsequently German Chancellor Scholz tried to reassure markets on Friday saying, "Deutsche Bank has fundamentally modernized and reorganized its business model and is a very profitable bank. There is no reason for concern."

Meanwhile, adding to uncertainty, Bloomberg News reported that Credit Suisse and UBS are among the firms under scrutiny in a US probe into whether bankers helped Russian oligarchs evade sanctions.

In the US, Treasury Secretary Yellen convened the heads of US financial regulators on Friday, calling for an unscheduled meeting of the Financial Stability Oversight Council. Secretary Yellen and regulators have come under pressure to give clarity to depositors in US regional banks regarding their uninsured deposits - ie whether these would be guaranteed as in the cases of SVB and Signature banks.

Chart: DB CDS, share price and STOXX Europe 600 banks index

On the US data front, there were no Tier 1 releases this week. The main event this week was the highly anticipated FOMC meeting. The banking sector turmoil began in the Fed's pre-meeting communication blackout period, so the market did not get any "signals" from FOMC participants as to how their views may have changed in light of the two bank failures.

The FOMC hiked its policy rate 25bps to 4.75%-5.00%. While a hike or a pause was much debated ahead of the meeting, the result was not a surprise in that the probability of the 25bp rate hike was over 80% priced in. Fed Chair Powell continued to emphasize the Fed’s inflation fight in the press conference, saying, “Without price stability, the economy will not work for anyone.”

Therefore, the Fed separated its inflation fight from its need to stabilize the banking sector, using different tools for each job. (Rate hike to counter inflation and the new lending facility, announced when SVB and Signature banks failed, for banking sector liquidity issues). We will see if the Fed can continue to proceed in pursuing these important mandates separately. The market does not think so, and expects March's rate hike to be the Fed's last in this hiking cycle (see Fed pricing section below). Thus, the market sees the Fed abandoning its inflation fight in the interest of banking sector stability. Our full FOMC review note is here.

Fed Pricing:

Fed funds futures have the peak in the terminal rate priced at 4.85% in May. As the Fed funds target range is 4.75-5.00%, this means that the rate hike the Fed delivered this week is expected to be the last in the cycle. The market has priced rate cuts post the May FOMC meeting through the remainder of the year and expects 100bps of rate cuts by year-end.

Contrast this pricing to pricing March 8 - the day before the SVB troubles came to light. On March 8, Fed funds futures priced the peak in the terminal rate at 5.69% in September and had only 13 bps of cuts priced by year-end. Expectations have turned around quite a bit since then in a dovish direction.

Chart: KBW regional bank index and KBW wider bank index underperform S&P500 recently.

Turning to the Diamond Commodity:

DIAMINDX fell 0.7% on the week to USD 5,360. In diamond industry news, Diamond Standard Director Neshiva Chan took a look at Petra Diamonds' rough tender:

Petra Diamonds announced positive data for their fourth tender for FY 2023. For background, Petra is in a group of the four most sizable diamond producers just beneath the three largest and is recognized as one of the most prominent miners in the industry. Its portfolio includes an open pit mine in Tanzania and three underground mines in South Africa, however, production at their Tanzanian mine remains suspended. A targeted restart in production for that mine is planned for Q1 FY 2024.

The results for the fourth tender for FY 2023 marked a 12.5% increase in like-for-like prices over the third tender. This implies further support to confirm solid demand and an improving price trend. Included in the sales were USD 7 million from Exceptional Stone sales discovered at the Cullinan Mine in South Africa. Cullinan Mine is well known for large high-quality diamonds as well as having sourced two of the largest diamonds in the Crown Jewels.

Richard Duffy, CEO of Petra Diamonds, pointed toward China's easing COVID-19 restrictions and the positive sentiment and demand at the Hong Kong International Jewelry Show. The HKTDC Hong Kong International Jewellery Show and the Hong Kong International Diamond, Gem & Pearl Show returned for the first time in three years after cancellations due to the global pandemic and saw strong interest with 2,500 exhibitors participating from 36 countries.

Gold Gold was down 0.6% on the week after last week's strong 6.5% gain. However, earlier on Friday as the market focused on the spike in DB's CDS, gold traded above USD 2,000 but retreated later in the day to end the week at USD 1,977.

Silver Silver gained 2.5% on the week, its second consecutive weekly gain, to come in at USD 23.17. Support is USD 23.00 and USD 24.00 has proven to be strong resistance.

__ In March so far, precious metals have benefitted from collapsing US yields, a weaker USD, and safe haven demand stemming from turmoil in both the US and European banking sectors__. Though US yields are lower, their moves have been highly volatile. (see MOVE Index here). Gold and silver have, to some extent, been moving around with these swings in US yields. The diamond commodity's price (DIAMINDX) less so. The chart below shows 30 day volatility of gold, silver and DIAMINDX. All of their respective vols have risen recently, but DIAMINDX has the lowest volatility.

The outlook for the US economy is uncertain in terms of recession timing. US banking sector turmoil is likely to continue near-term as depositors mull whether to pull their deposits out of regional banks. As a result, we continue to expect periods of sharp risk aversion ahead. We see the benefit of precious metals in a portfolio to hedge against periods of distress and specifically the benefit of the diamond commodity in a portfolio given its low volatility and very low correlation with other asset classes. (see more commentary here).

Chart: DIAMINDX, Gold, and Silver Volatility (30 day). DIAMINDX has the lowest vol.

__ USD modestly lower__

USD was down a modest 0.5% this week. The DXY Index remains in a 102.00-105.65 trading range. Support is at 102.00 and resistance at 103.45 (50 day movg and 104.00). The US 2 year yield moving lower weighed on the DXY (chart below). Risk seeking Dollar-Bloc currencies (AUD, NZD, CAD) were the worst performing vs USD on the week. EURUSD gained 0.8%. NOK was the strongest performer vs USD in the G10 this week, rising 1.9% after Norges Banked hiked 25bps, signaled more to come, and said that they expect NOK to appreciate "somewhat".

Chart: USD (DXY Index) vs US 2 year yield - lower 2yr yield weighs on USD.

__Ahead - select events: __ The Fed takes center-stage once again with Vice Chair for Supervision Barr's testimony on Bank Oversight. Fed Chair Powell was asked about the failings of SVB at the FOMC press conference and he deferred to Barr's investigation and upcoming testimony.

Monday, March 27

- BoE Gov Bailey speaks at London School of Economics

- Germany IFO (Mar)

- Fed Gov Jefferson (voter) speaks: Implementation and Transmission of Monetary Policy

Tuesday, March 28

- US Conference Board Consumer Confidence (Mar)

- Testimony -- Fed Vice Chair for Supervision Michael S. Barr on Bank Oversight Before the U.S. Senate Committee on Banking, Housing, and Urban Affairs

Wednesday, March 29

- BoE's Mann speaks on "Inflation and Monetary Policy" panel

- Testimony -- Fed Vice Chair for Supervision Michael S. Barr on Bank Oversight Before the U.S. House Financial Services Committee

Thursday, March 30

- Germany CPI (Mar)

Friday, March 31

- Eurozone CPI (Mar)

- US PCE prices (Feb)

- Speech -- Fed Gov Waller (voter) "The Unstable Phillips Curve"

- Speech -- Fed Gov Cook (voter) The U.S. Economic Outlook and Monetary Policy

Sign Up for Market Commentary: Weekly insights on global markets and commodities from Diamond Standard by Amelia Bourdeau

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.