Market Update: Hike or Pause

US equity indexes were up on the week: S&P500 1.0%, NASDAQ 2.0%, and DJIA 0.7%. Equity indexes were buoyed by solid US economic data and the possibility that the Fed and other global central banks are nearing the end to their tightening cycle. This week, both the Fed and the ECB signaled that they could hike or pause at their September policy meetings. Currently, the US soft landing narrative is the dominant market theme.

July FOMC and US economic data:

The FOMC hiked the policy rate by 25 basis points to 5.25-5.50% - as expected. This is the highest level in 22 years.

In the press conference, Powell noted the FOMC will make decisions meeting by meeting, remaining data dependent. Powell said specifically that the Fed could hike or pause in September. Between now and the September meeting, eight weeks, the Fed will get key employment and CPI reports. Powell chalked up the most recent CPI release (June), which came in under expectations, to being just one month of data.

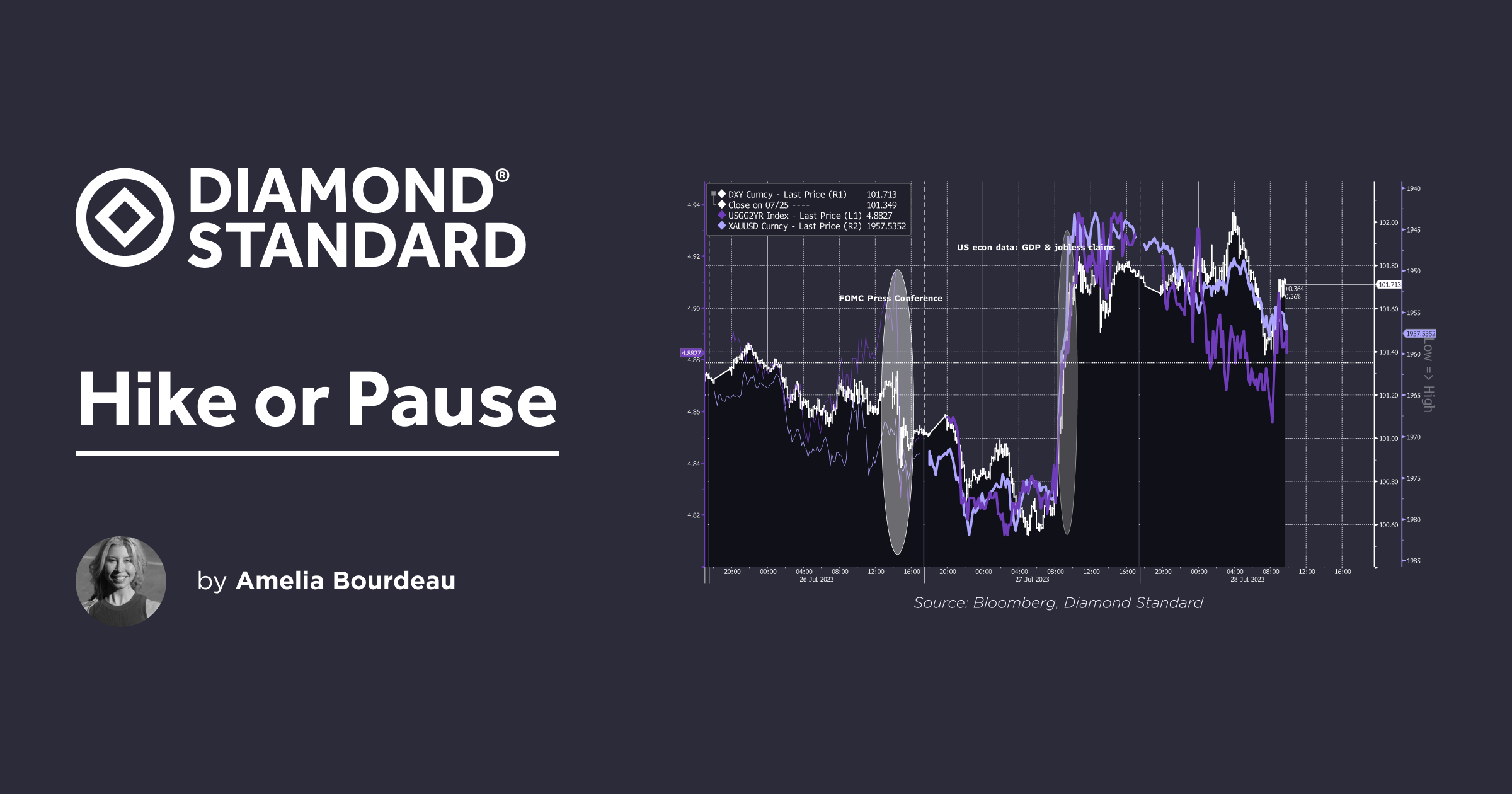

Market participants on Wednesday afternoon ("Fed day") focused on the message that a pause was possible in September. The US 2 year yield fell, gold rose and USD was lower intraday in reaction to the press conference.

However, better than expected US economic data released on Thursday - US Q2 GDP and initial jobless claims - reversed that price action (chart below). US GDP in Q2 was stronger than expected at 2.4%q/q, ar (est. 1.8%). Within the report, personal consumption rose 1.6% (est. 1.2%). Weekly initial jobless claims came in on the low side at 221k (est. 235k).

Fed Pricing

The peak in the fed funds rate is priced as November at 5.41%. Market pricing has converged to the Fed's forecast of no rate cuts this year. Fed fund futures are pricing in a 22% probability of a 25bp rate hike in September.

Chart: Intraday USD (DXY Index), Gold and US 2 year yield. Reaction Wednesday to "Fed could pause" and Reaction Thursday to strong US economic data = "Fed could hike"

Precious Metals:

Precious metals investors are keeping an eye out for the peak fed funds rate, which they hope will be followed quickly by a "pivot" in the Fed's narrative on inflation (to less hawkish) and, as a result lower, US yields and further USD decline - all of which would support precious metals prices. As we noted in last week's WIR, fed funds futures are pricing rate cuts commencing earlier in 2024 than the fed's forecast and more of them. The risk is that market participants, once again, revise their expectations and pricing toward the fed's more conservative rate cut forecast.

Given the uncertainty in the US economic outlook, we continue to see the need for an allocation to precious metals in a portfolio both as a safe haven investment and for diversification to hedge against macro risk.

DIAMINDX fell 1.3% on the week to USD 4,740. DeBeers Group released its Cycle 6 results for rough diamond sales. Cycle 6 sales came in at USD 410 million, which is down 10% from Cycle 5 and down 36% from Cycle 6 2022. IDEX online reported that "Prices of stones over 2-cts were reportedly reduced by as much as 20 per cent at the sight in Gaborone earlier this month."

Al Cook, CEO, De Beers Group, said: “In line with seasonal trends, rough diamond sales continued at a lower level during the sixth sales cycle of the year. Participants in the diamond industry’s midstream sector continue to take a cautious approach to purchases in light of ongoing macroeconomic challenges.” However, from a consumer jewelry standpoint, it is encouraging that so far US economic growth and the job market remains relatively robust.

Chart: DeBeers Group Rough Diamond Sales

Gold fell 0.2% on the week to USD 1,958. Gold was temporarily boosted on Wednesday with Powell indicating the option of a September pause, but fell 1.3% on Thursday with the release of stronger US economic data which supported US yields. USD 1,960 is resistance for gold. Silver fell 1.4% on the week to USD 24.26, impacted by the same forces as gold. Support is USD 24.00.

Looking ahead, gold and silver are likely to be impacted more by movements in the US 10 year yield, the back end of the curve. Front-end US rates seem comfortable pricing that the peak fed funds rate is near. The changing economic outlook is what is creating volatility for longer-term US yields and precious metals.

Chart: US 10 year yield (inverted), gold and silver - intraday 1 week. Moving together.

__USD __

The USD (DXY Index) rose 0.6% on the week to 101.70 at the time of writing. The USD gained against all G10 currencies except the JPY (see below) for its second consecutive weekly gain. The DXY Index has been in a range of 106.00-100.00 since the start of the year. It has been sub -102.00, which is resistance, since last week's release of the weaker than expected US June CPI.

The ECB hiked its policy rates 25bps as expected (refinancing rate to 4.25%, marginal lending rate to 4.50% and deposit rate to 3.75%). Similar to Powell, ECB President Lagarde said that policymakers could decide between a hike or a pause in September - a bit of a less hawkish stance than previously. EURUSD fell 1.4% during the press conference sub -1.1000 to 1.0990. It ended the week approximately 0.8% lower at 1.1031.

JPY gained initially vs USD on Thursday on a Nikkei news report that the BoJ would discuss tweaking its yield curve control policy a its policy meeting on Friday. At that policy meeting, the BoJ did indeed say that it would offer to buy 10-year JGBs at 1.0% in fixed-rate operations, instead of the previous rate of 0.5% - tolerating the wider band. All in all, JPY was the strongest G10 currency vs USD on the week, rising 0.8%.

Chart: USD (DXY Index) Ranges

We recently sat down on our podcast Clarity with Chris Marsh, Chief Economic Advisor - Exante Data, for a conversation on inflation. His views are always informative. Links here to listen.

Ahead next week: The main release is US July payrolls on Friday - consensus expects a gain of 185k. US ISM readings will also be released. The BoE has a monetary policy meeting and press conference.

Sign Up for Market Commentary: Weekly insights on global markets and commodities from Diamond Standard by Amelia Bourdeau

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.