Market Update: Not Done Yet

US equity indexes were up on the week: S&P500 2.6 %, NASDAQ 3.2%, and DJIA 1.2%. This week was the S&P500's best weekly performance since the end of March. Despite a more hawkish Fed than expected (see below), US equity markets focused on the fact that the Fed is nearing its terminal rate. Equity indexes are also being boosted by continued positive AI sentiment and by growing expectations that China will provide a package of economic stimulus measures post the PBOC's rate cut in its short and medium term policy rates.

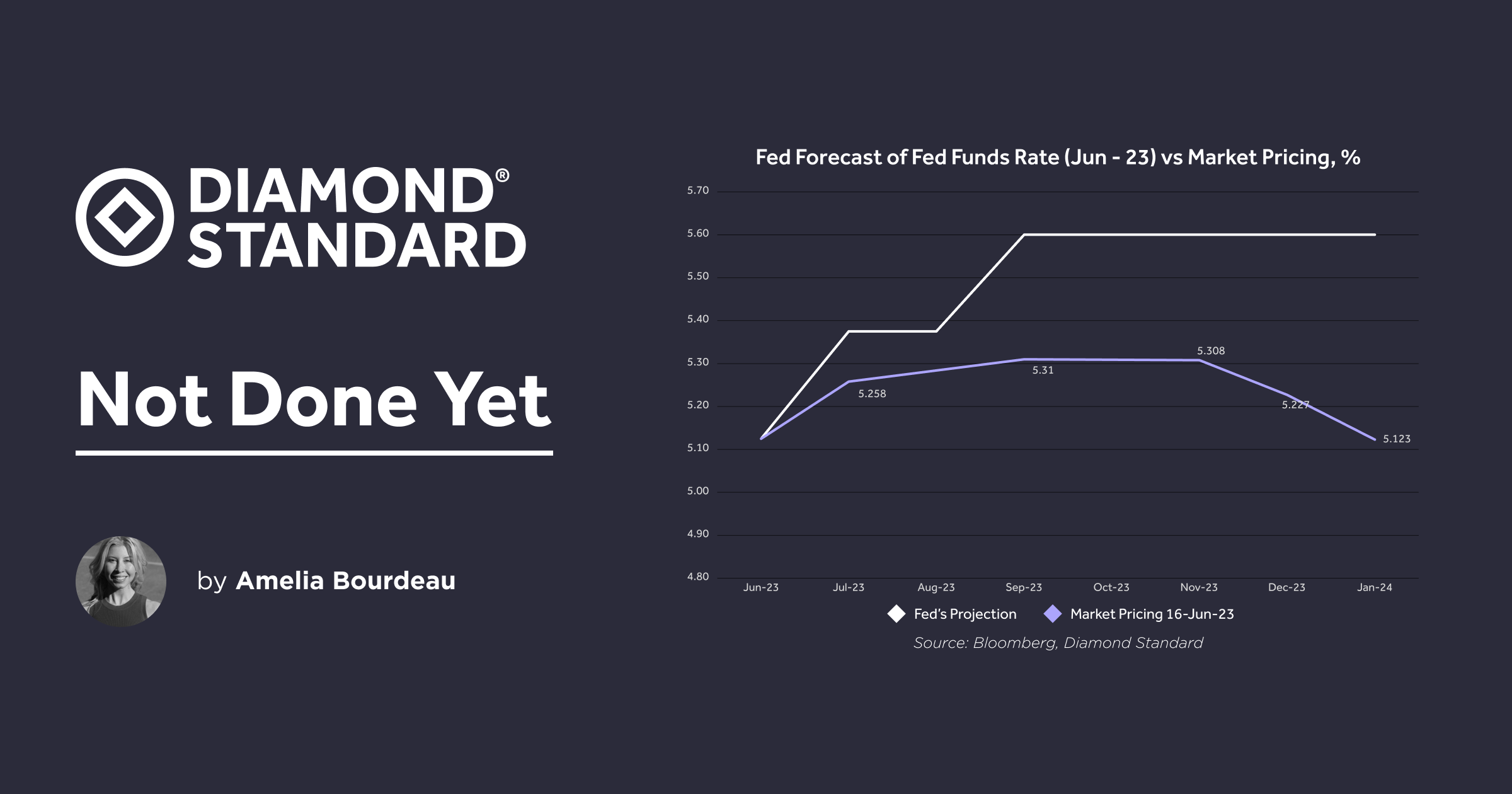

Fed Pricing:

The FOMC announcement and new forecast release were more eventful than anticipated. The Fed held rates steady at 5.00-5.25% as expected. This is the first time in 15 months that the Fed has not raised its policy rate. While market participants expected a "hawkish pause", the FOMC was more hawkish than expected. Its June Summary of Economic Projections ("SEP") showed the median Fed Funds Rate was forecast to be 5.6% at year-end vs 5.1% in the previous forecasts (March SEP). The Fed is assuming two more rate hikes this year vs only one that market participants were partially pricing in prior to the release of these forecasts.

Fed Chair Powell, in his press conference, said that nearly all committee members view it likely that further rate hikes will be needed to bring inflation to 2% target by the end of the year. In addition, Powell noted that he expects that "July will be a live meeting."

According to fed fund futures pricing, the peak in the fed funds rate is now September at 5.31%. Only 18 bps of rate cuts are expected by January 2024 indicating that market pricing doesn't fully believe the Fed's new forecast of two more 25bp rate hikes. However, market pricing has been converging to the Fed's forecast and narrative of no rate cuts this year.

Chart: Fed's Rate Forecast (June 2023) vs Market Pricing (assumption: spreads out the 50bps of hikes in July and September)

Precious Metals:

DIAMINDX was unchanged on the week at USD 5,100. It continues to hold above the USD 5,000 level. We take a look at US retail sales as a proxy for the health of the consumer as the US is the world's largest market for diamonds. US retail sales for May, released this week, surprised to the upside for the headline, which gained 0.3% m/m and were on expectations for the ex autos read, rising 0.2% m/m. While US consumers are still spending, momentum is slowing.

Signet jewelers, the world's largest retailer of diamond jewelry recently released its results for "first quarter fiscal 2024" which are the 13 weeks leading up to the end of April 2023. Sales were down 9.3% y/y and same stores sales fell 13.9% y/y. Signet cited "a softer than expected Mother's Day increasing macro-economic pressures on consumers at more price points, and deeper competitive discounting" as the reasons for the deceleration in trends.

In addition, Signet CEO Virginia Drosos noted in a press release that "In line with our predictions, there were fewer engagements in the quarter resulting from COVID's disruption of dating three years ago." US engagement ring sales are approximately 25% of the global market for diamonds and act as an indicator of the strength of diamond sales.

In industry news, JCK online's Rob Bates has an updated report on Russian sanctions. Currently, the US allows the import of Russian-mined gems if they have been polished elsewhere (substantially transformed). However, at the latest G7 meeting, leaders moved towards further sanctioning Russian diamonds but did not give any details.

Bates reports that sources who spoke with government officials from the US and Belgium at the JCK show recently in Las Vegas expect that new rules for sanctions will start in January 2024. "At first, the regulations may be limited to diamonds 1 ct. and larger. The minimum weight could progressively decrease as time goes on, possibly at six-month intervals..Customs will require importers to declare their diamonds aren’t from Russia, but will not ask for other info about the diamond’s origin," reports Bates. It is not known yet what documentation will be required. Any further sanctioning of Russian diamonds will constrain supply to Western countries.

Gold and Silver

Gold was flat on the week to come in at USD 1,959. Gold had conflicting influences impacting it. The movement up in the US 2 year yield and fed fund futures expectations weighed on gold mid-week. However, the weakening in the USD post the ECB rate hike and hawkish talk by President Lagarde on Thursday (see USD section below) helped to support gold into the end of the week. Gold ranged USD 1,970 - USD 1,925 this week.

The chart below shows the fed funds futures January 2024 contract vs gold. The volatility in the pricing of the Fed outlook has been impacting gold - moving it around shorter-term.

In addition to gold grappling with the influences of both higher US rates (negative) and a weaker, though not weak, USD (positive), other factors are at play as well. The US debt ceiling uncertainty has passed and there has not been any recent bank failures, so the need for safe haven investment is less in the immediate sense. Looking ahead, it seems as if the peak in the fed funds rate is nearing, which is a plus for gold. Economic and geopolitical risk remain and when/if these market themes move to the forefront. These risks should be supportive for gold as well. Strong central bank gold buying has underpinned the price, but we will need to see whether that continues and will need to see more participation from institutional investors to propel gold to its highs again. With risks on the horizon, portfolios can benefit from the diversification precious metals offer.

Silver fell approximately 1% on the week to come in at USD 24.04 - holding above support at USD 24.00 and at USD 23.80. This week's drop followed two weeks of strong gains. Silver has been trading in a range of USD 22.70 - 24.50 since mid-May.

Chart: US fed funds future Jan-2024 vs Gold (inverted). The move up in the expected policy rate, has capped gold.

Since market participants are, once again, focusing on the terminal rate, the chart below looks at DIAMINDX, gold, and silver during those times back to 2002. Post the peak in the fed funds rate during the last two rate hiking cycles, into the rate cutting cycles and recessions that followed (December 2007 - June 2009 and February - April 2020), gold rallied, while DIAMINDX and silver fell. This makes sense give gold's safe haven properties vs silver's industrial component and diamonds' reliance on consumer spending both of which are negatively impacted by recession. DIAMINDX begins to turn up a couple of months post the end of the recession.

__Chart: Fed Funds Rate, DIAMINDX, Gold, and Silver. Recession periods shaded. __

USD

The USD (DXY Index) was on its backfoot this week, falling 1.4%. A rate hike and hawkish tone from the ECB at its policy meeting announcement on Thursday, boosted EUR (the DXY Index's largest component). Despite the hawkish tone from the Fed, it left the policy rate unchanged this week, while the ECB hiked 25bps - hence the reaction in EURUSD. EURUSD rose 1.2% during the ECB press conference, breaking topside resistance levels 1.0850 and 1.0900. EURUSD was up nearly 2% on the week to end at 1.0950.

Throughout Thursday post the ECB press conference, the DXY Index fell from 103.25 area to 102.11. At the time of writing, USD (DXY Index) is holding just above support at 102.00.

__Chart: DXY Index and EURUSD - oval is ECB announcement / press conference on Thursday. __

__ Ahead next week:__

Monday is a US federal holiday - markets are closed. On Wednesday, market participants will be focused on Fed Chair Powell's Semiannual Monetary Policy Report testimony to Congress before the US House Financial Services Committee. On Wednesday as well, there will be testimony from Fed Gov Cook and Jefferson at their nomination hearings.

UK CPI for May will be released. The BoE will announce its policy rate decision - the Bloomberg consensus expects a 25bp rate hike.

Institutional Media: We launched our new Diamond Standard podcast Clarity last Friday. In Episode Two, we are joined by Bill Kelly, President and CEO of CAIA Association. This wide-ranging conversation covers: a new take on the 60-40 portfolio, liquidity and ALTS investing, the portfolio of the future, and the individual investor and ALTS investing. You can catch the podcast on Spotify and Apple podcasts and on our Diamond Standard institutional media page.

Sign Up for Market Commentary: Weekly insights on global markets and commodities from Diamond Standard by Amelia Bourdeau

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.