Market Update: Price Pressure

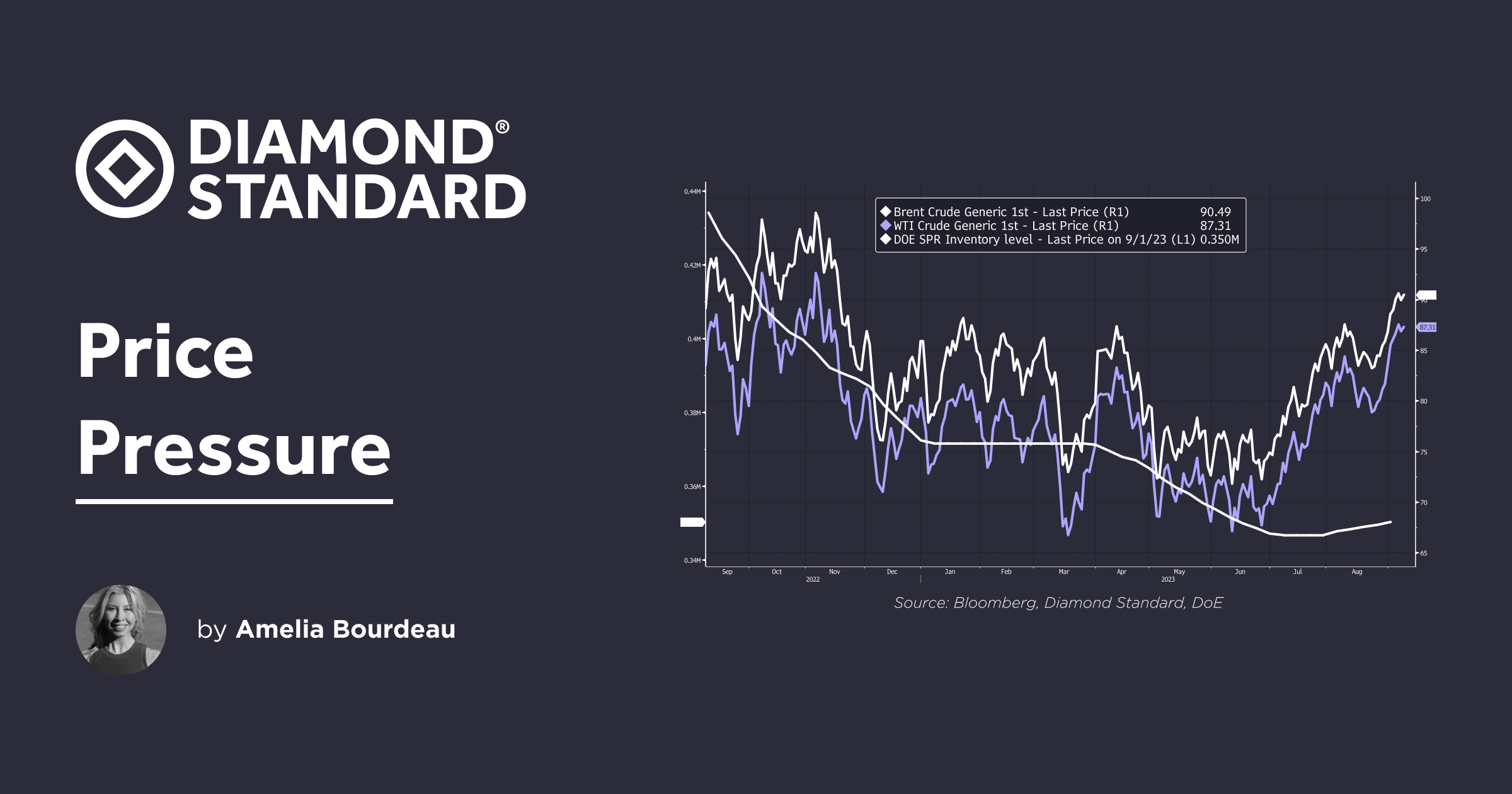

US equity indexes were down on the week: S&P500 -1.3%, NASDAQ -1.9%, and DJIA -0.7%. The focus this week was on renewed price pressure as Saudi Arabia and Russia announced they will extend their voluntary oil production cuts of 1 million barrels per day another three months through the end of this year. This lifted Bent crude oil above USD 91 per barrel - the highest since November. Rising oil prices could complicate the Fed's inflation fight. US bond yields nudged higher. US consumers hoping for relief from high gasoline prices at the pump could be disappointed. President Biden has used the Strategic Petroleum Reserve ("SPR") to relieve price pressure previously. However, the SPR has been drawn down quite a bit all ready (chart below).

Fed Pricing:

Market participants continue to expect a pause in the hiking cycle at the September FOMC meeting. However, the Fed is not in the clear yet as oil prices are rising and employment is slowing but still robust. The US ISM Services Index, released this week, surprised to the upside showing that the services sector was strong. Market participants are considering how long the policy rate will stay at a high level. The peak in the fed funds rate is priced as November at 5.44%. There are approximately 110bps of rate cuts priced in for 2024. Stronger growth in 2023 may cause sub-par growth in 2024.

Chart: WTI, Brent, DoE's Strategic Petroleum Reseve Inventory

Precious Metals:

Gold and silver remain capped due to high US bond yields and a strong USD. Precious metals would benefit from a dovish pivot in Fed language - signaling rate cuts are ahead. However, the US economy seems headed for a soft landing in 2023 so far and as seen this week, the rise in oil prices complicates the inflation fight.

The diamond industry is in the midst of an inventory overhang at the manufacturing and retail levels. Contributing factors are: softer US consumer spending on diamond jewelry after an aggressive run up in 2021-2022, a sharp slowdown in China's economy, and some competition from lab-grown diamonds. On a positive note, the US economy continues to avoid recession - this supports the US consumer into year-end and the holiday shopping season when diamond sales are seasonally stronger.

From a portfolio standpoint, with geopolitical risk, the timing of a US economic slowdown being fluid, the possibility of a miscalculation in the calibration of Fed policy, and a US election year ahead, we continue to see an allocation to precious metals as both necessary and beneficial from diversification and safe-haven stand-points.

DIAMINDX fell 0.8% on the week to USD 4,480. Last week, we discussed the disappointing DeBeers Group Cycle 7 rough diamond sales and some of the diamond market dynamics around inventory accumulation among the manufacturers and retailers.

This week, Rapaport News reported that India's Gem and Jewellery Export Promotion Council ("GJEPC") "will ask diamond miners to be sensitive to the needs of the industry amid concerns over an inventory imbalance." India is a major cutting and polishing center for diamonds. GJEPC chairman Vipul ShaIf said "if the market situation doesn’t improve after the Jewellery & Gem World show in Hong Kong later this month, 'further actions [will] need to be taken.' "

However, not all is negative in the diamond jewelry industry. Signet Jewelers ("Signet") recently reported its Q2 fiscal 2024 results (quarter end July 29, 2023) and beat earnings estimates. For background, Signet is the world's largest retailer of diamond jewelry. Signet operates primarily under the name brands of Kay Jewelers, Zales, Jared, Banter by Piercing Pagoda, Diamonds Direct, Blue Nile, JamesAllen.com, Rocksbox, Peoples Jewellers, H.Samuel and Ernest Jones.

Sales came in at USD 1.6 billion, down 8.2% on a constant currency basis from Q2 of FY23 (year-on-year). This result beat the analyst consensus estimate of sales of USD 1.58 billion. Same store sales ("SSS") excluding Blue Nile were down 12.0% to Q2 of FY23. Adjusted EPS of $1.55 beat the analyst consensus estimate of $1.45. On another positive note, Signet said it reduced inventories by 4% from the prior year and 8% excluding acquisitions.

"We remain confident in our ability to achieve our Fiscal 2024 guidance," said Signet CEO Virginia C. Drosos. "Our reimagined merchandise assortment and upcoming holiday season initiatives will leverage our investments in innovation, digital capabilities, and data analytics to widen our competitive advantages. We believe the upcoming multi-year recovery of engagements [re: engagement ring sales] remains on track to begin in the fourth quarter of this year."

Included in Signet's Q3 and full year Fiscal 2024 outlook is the assumption that it expects "US Jewelry industry revenues to be down more than the Company's initial expectations of mid-single digits, driven by the impacts of macroeconomic factors on consumer spending and continued shift of consumer discretionary spend." So, while Signet sees the US consumer slowing down or shifting spending perhaps toward services, ahead the Company sees a multi-year recovery in engagements and therefore bridal jewelry sales starting in Q4.

Gold and Silver

Gold fell 0.7% this week to USD 1,927. Silver fell 4.4% on the week to USD 23.13. Support is USD 23.00, 22.25, and major support at 22.00. The gold-to-silver ratio rose to 83.4 this week from 80.2 last week. It has been cycling between 85 - 78 since the start of July.

Turning to gold, the World Gold Council ("WGC") reported that central bank gold buying was up in July (the latest data). Central banks added 55t to global gold reserves for the month, led by China and Poland. Both of those countries added about 23t to their reserves. The WGC noted, "Looking at the detailed activity during July, two things are notable: 1) relatively few banks altered their gold holdings in July, and 2) many that did buy/sell did so sizeably." The Central Bank of Turkey bought 17t in July following on from 11t in June, but remains a net seller year-to-date. WGC reported that gold ETFs had another month of outflows in August. "AUM fell US$3bn (46t), with the majority coming from US listed funds."

Chart: DXY Index, US 10 year yield, Gold (inverted) and Silver (inverted)

USD

USD (DXY Index) was up 0.6% on the week to 104.85 at the time of writing. This is the eighth consecutive week of USD gains. The US economy on a relative and absolute basis is outperforming, which is supporting the USD.

Since the start of September, EURUSD has shifted lower - breaking downside support at 1.0800. The single currency has been trading in a narrow 1.0750-1.0700 range throughout the week. USDJPY is at 147.38 at the time of writing - remaining near levels of MoF intervention last fall.

Chart: USD (DXY Index) and WTI Crude Price

Ahead:

India is hosting the G20 meeting this weekend. Next week, all eyes will be on US CPI for August, which is expected to rise at the headline and remain steady for the core reading on a month-on-month basis. In addition, US retail sales for August will be released along with U of Michigan consumer sentiment for September preliminary read. There is an ECB monetary policy meeting. Market participants are divided about whether they hike or pause, so the policy meeting outcome could move the Euro.

The Week In Review is on hiatus next week and will resume September 24th.

Sign Up for Market Commentary: Weekly insights on global markets and commodities from Diamond Standard by Amelia Bourdeau

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.