Market Update: Shiny Ball

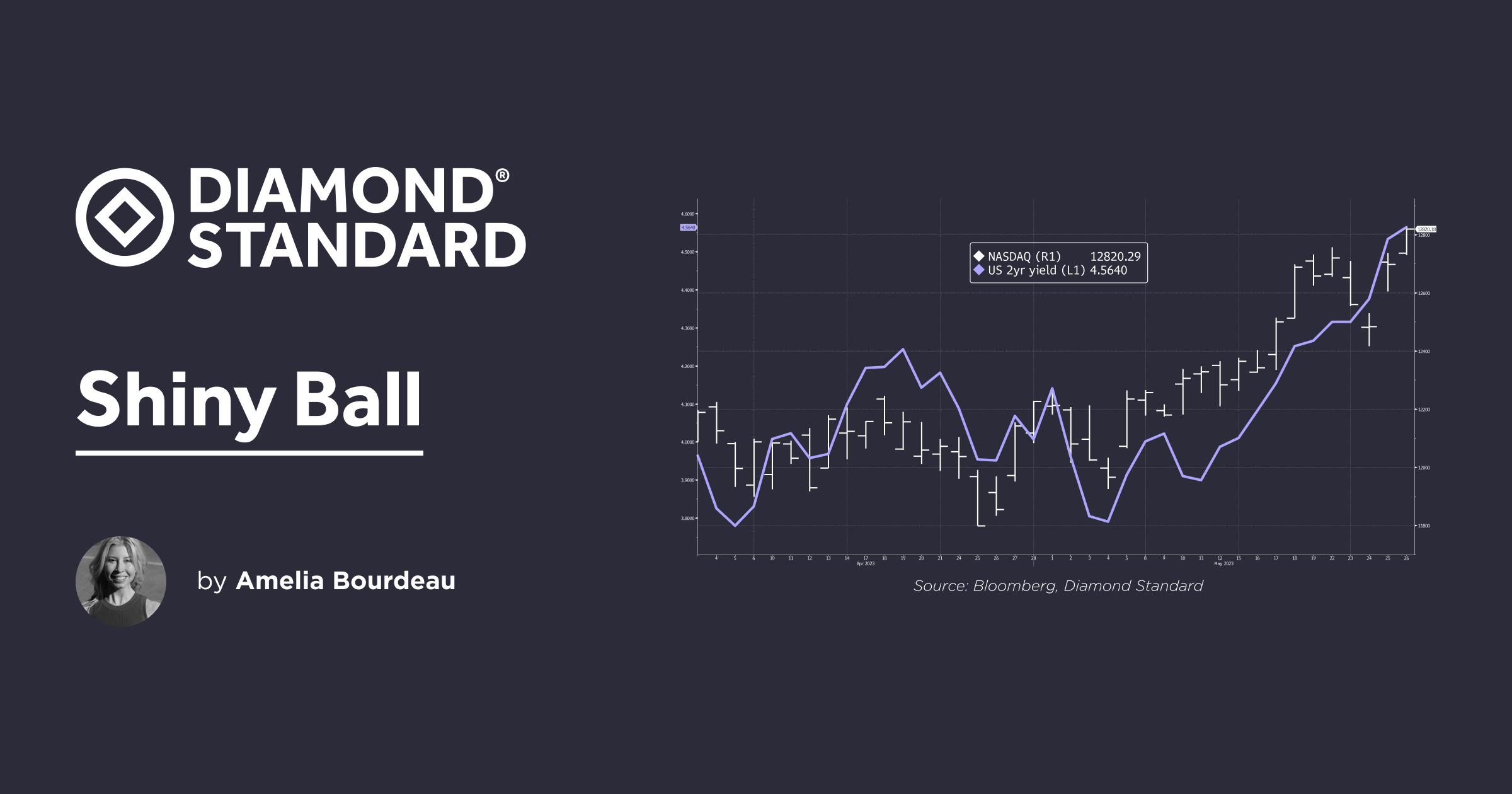

US equity indexes were mixed this week: S&P 500 0.3%, NASDAQ 2.5%, and DJIA -1.0%. Market action this week was shaped by two competing forces - US debt ceiling concerns and AI euphoria post Nvidia's bullish sales forecast. Fitch placed the US's 'AAA' long-term rating on rating watch negative, but US equities continue to focus on the shiny ball that is big tech. It is a headline driven market, so trading conditions remain choppy. Managing Director Amelia Bourdeau talks to Real Vision here about the market's dueling influences and moves this week.

Fed Pricing:

May FOMC minutes showed that participants agreed that a pause in the rate hiking cycle was needed (this was pre this week's higher inflation data) but did not agree on whether the current fed funds rate was the peak rate, meaning some participants thought there could be further rate hike(s). However, no FOMC participants saw a rate cut ahead.

On Friday, US PCE prices were released for April. PCE Prices accelerated at both the headline and core readings on a year-on-year basis. As a result, US bond yields rose and the probability of a Fed rate hike in June increased.

Fed funds futures show a growing probability (58%) of a 25bp rate hike in June and 26% of an additional 25bp rate hike at the July meeting. The peak in the terminal rate is now July and fed funds futures have approximately 50bps of rate cuts priced in by the end of January 2024 - less than last week.

Chart: NASDAQ higher and US 2yr yield higher

Precious Metals:

DIAMINDX was unchanged on the week at USD 5,110. It continues to hold above the USD 5,000 level.

In industry news, Petra Diamonds reported its sales value at its fifth rough tender were down both from tender four, which saw strong sales, and on a year-on-year basis. Sales were down 51% from the fifth tender a year ago and down 42% from tender four, which ended in March. In the fifth tender, 468, 817 carats were sold for USD 42.1 million. This included one exceptional stone - a 354.04 carat near-gem quality stone that sold for USD 5.6 million. There were no sales for either Koffiefontein or Williamson mines in this cycle given the suspension of operations at both.

Petra's release noted that "The softer demand is attributed to inventory levels in the midstream and extended shutdowns by certain manufacturers following the recent Indian holidays. With the extended holidays set to end in the coming weeks, demand is expected to improve..."

On the outlook, CEO Richard Duffy said: "We continue to see a supportive diamond market in the medium to longer-term as a result of the structural supply deficit, despite the volatility seen in this current sale."

Ahead, is the JCK trade show in Las Vegas June 1-5. Diamond Standard will attend. It is one of the largest jewelry conventions on the world and will be important to gauge demand and the state of the industry.

Chart: Monthly Returns: DIAMINDX and Gold & Silver average. USD weakening late 2022 helped propel gold and silver. A rise in rates and the USD of late have weighed on them. DIAMINDX has been moderating toward pre-pandemic 2019 levels.

Gold and Silver

Gold fell 1.6% on the week to USD 1,945, breaking support at at USD 1,950. Support is now USD 1,935. Resistance is USD 1,993 and larger at USD 2,000. US economic data this week showed signs of resiliency and the latest inflation read was sticky. US bond yields moved higher and the market priced in more Fed rate hikes - factors that led to a third consecutive weekly loss for gold. The US bond market remains volatile with the looming US debt ceiling. This volatility is impacting gold. A resolution to the debt ceiling brinkmanship in the near term (Treasury Secretary Yellen on Friday said the X-date is now June 5) could weigh on gold further - but a swift resolution is no guarantee.

In news out of the World Gold Council: the latest Gallup Poll Social Series, which monitors public opinion on economy and finance, shows that gold jumped into second place as ‘best long-term investment’ in the US this year. The number one investment was real estate.

Silver fell 2.6% on the week to USD 23.26, breaking support at USD 23.40. This is silver's third consecutive week of decline. From a macro perspective, it is falling for the same reasons as described above for gold. Support comes in at USD 22.00 and resistance at USD 23.37 and USD 24.00.

Chart: Gold, Silver and the US 10 year yield (purple, inverted). A higher US yield dragged gold and silver lower.

__USD __

The USD (DXY Index) gained 1% on the week, rising to 104.29 at the time of writing. The DXY broke topside resistance at 104.00. USD has been trending higher since mid-May when it broke out of its narrow 102.40-101.00 trading range. The USD gained against all G10 currencies this week.

The DXY's largest component, EUR fell 0.8% on the week to 1.0720. EURSD is likely to remain under pressure as market participants are now pricing a more hawkish Fed. On a side note, June 1 is the 25th anniversary of the ECB. "Whatever it cakes", right? Here is President Lagarde cutting the celebratory cake.

The UK had some bad news on the economic data front this week. UK April CPI surprised to the upside, coming in at 8.7% y/y vs expectations 8.2% y/y. Core CPI ticked up from 6.2% to 6.8% y/y. This is an ugly print. In reaction, UK bond yields moved sharply higher - back to where they were when former PM Liz Truss released an ill advised mini-budget back in September 2022. GBPUSD fell 0.8% to 1.2344.

Chart: USD (DXY Index) and recent trading ranges (rectangles) vs US 2 year yield.

Ahead next week:

The main release is US May payrolls on Friday, June 2. The Bloomberg consensus expects +178k vs +253 for the April read. Prior to that release, the market will be focused on ISM Manufacturing for May and ADP employment for May.

Note, the Week In Review is on hiatus next week and will resume June 9th.

Sign Up for Market Commentary: Weekly insights on global markets and commodities from Diamond Standard by Amelia Bourdeau

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.