Week in Review: Slower Pace

US equity indexes up on the week: S&P 500 1.5%, finishing above the 4,000 level for the first time in two months, NASDAQ 0.7% and DJIA 1.8%. Equity markets were supported by indications that the Federal Reserve is open to slowing its pace of rate hikes (see below). It was a holiday shortened week, with US equity and bond markets closed on Thursday for the thanksgiving holiday.

The National Retail Federation expects an estimated 166.3 million people to shop in the US from Thanksgiving Day through Cyber Monday this year. This figure is approximately 8 million more people than last year and is the highest estimate since NRF began tracking this data in 2017. NRF President and CEO Matthew Shay said, "We are optimistic that retail sales will remain strong in the weeks ahead, and retailers are ready to meet consumers however they want to shop with great products at prices they want to pay.”

On Wednesday, the November FOMC minutes were released. The staff noted that a US recession was almost as likely as the baseline forecast, FOMC participants are concerned that long term inflation expectations are above 2%, participants also noted that there is a high level of uncertainty around the terminal Fed Funds rate and that slowing the pace of of rate hikes "would likely be soon appropriate." The market focussed on the last comment and US equity indexes rallied. On the day, the US 2 year yield fell to 4.47% from. 4.51% and the US 10 year yield 3.69% from 3.75%.

Key points included:

On growth: "The staff...viewed the possibility that the economy would enter a recession sometime over the next year as almost as likely as the baseline."

On inflation: "Several participants expressed the concern that the longer inflation remained well above the 2 percent goal, the greater the risk that longer-term inflation expectations could become unanchored."

On the terminal rate: "Many participants commented that there was significant uncertainty about the ultimate level of the federal funds rate needed to achieve the Committee’s goals and that their assessment of that level would depend, in part, on incoming data...their assessment of the ultimate level of the federal funds rate that would be necessary to achieve the Committee’s goals was somewhat higher than they had previously expected."

On slowing the pace of rate hikes: "A number of participants observed that, as monetary policy approached a stance that was sufficiently restrictive to achieve the Committee’s goals, it would become appropriate to slow the pace of increase in the target range for the federal funds rate. In addition, a substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate."

Ahead, November 30th is the highly anticipated speech by Fed Chair Jerome Powell on the topic: The economic outlook and the labor market at the Brookings Institute. Market participants will look for confirmation from Powell of the November FOMC meeting minutes commentary that seems to suggest that the next rate hike could be 50bps as opposed to 75bps at the December 14 FOMC meeting. Currently, out of 87 economists surveyed by Bloomberg, 82 expect a 50bp rate hike, three expect a 75bps hike, and two expect a 25bp hike for that December meeting. Also ahead, on Friday, November US payrolls are released. The Bloomberg consensus expects a rise of 200k, down slightly from October's gain of 261k.

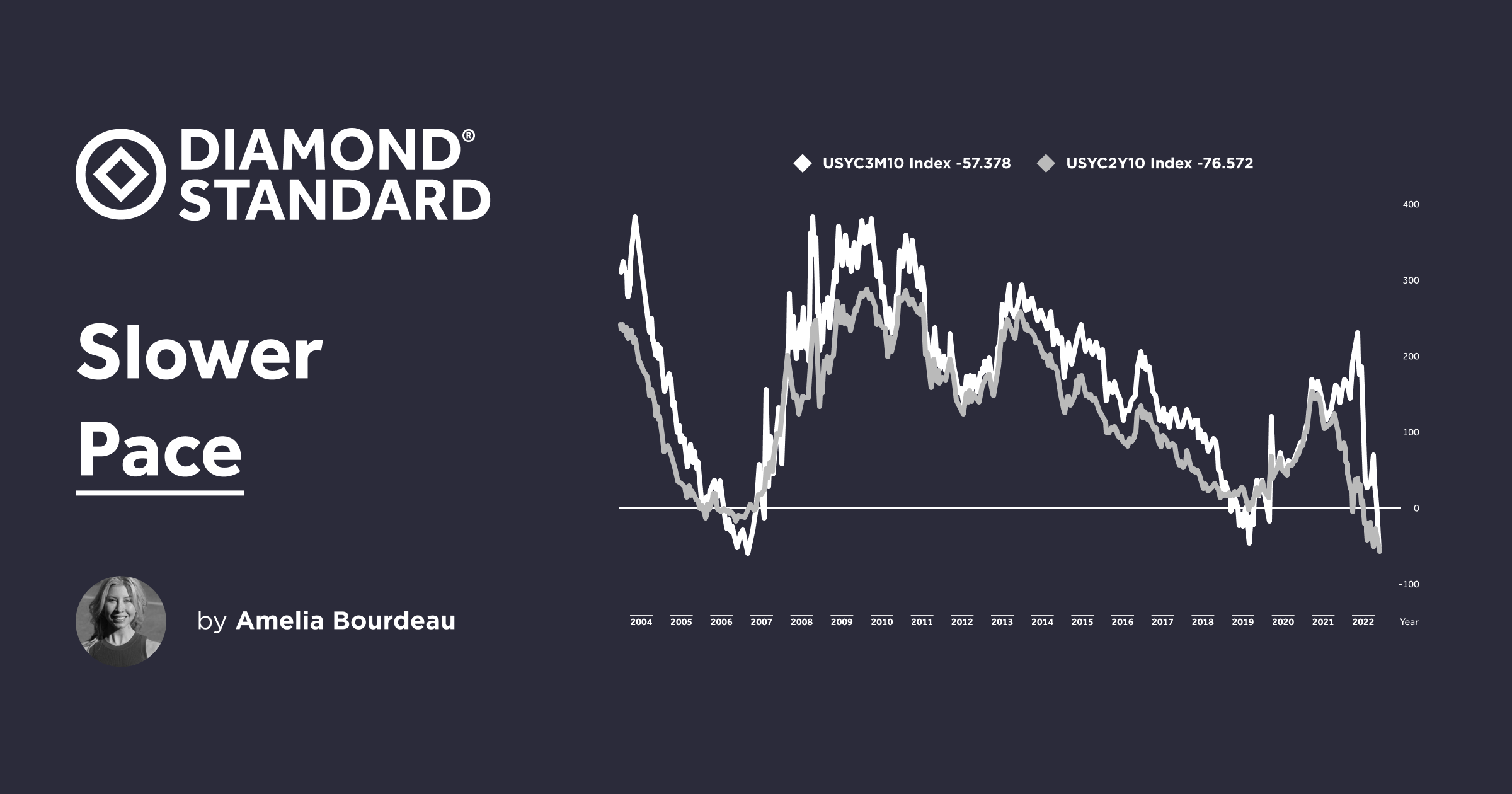

Chart: US yield curves 2s10s and 3mo10yr invert further. This signals a recession is likely but does not indicate a timeframe.

USD Weaker USD

USD (ie the DXY Index) is being largely driven by Fed-speak and the reaction of US yields. With US yields lower and equity indexes higher, the mild risk-seeking sentiment had the USD was on its back-foot. The DXY fell 0.9% on the week and has been ranging 108.00-105.55 since mid-November. EURUSD ranged 1.0250-1.0450. ECB Minutes showed that there was a debate on whether to hike 50bps or 75bps in October with "a very large majority" favoring 75bps, which was delivered. Looking ahead to December, the ECB seemed less hawkish. USDJPY continues to follow the US 10yr yield lower (chart), ending the week at 139.19. GBP has gained 5.7% vs USD so far this month. Sterling was at 1.2092 at Friday's close - a remarkable comeback from its mid-September low of 1.0350 when the UK changed Prime Ministers twice during the month.

Chart: USDJPY vs US 10 yr yield. Lower US 10 yr yield weighs on USDJPY.

Diamonds and Precious Metals

DIAMINDX fell 0.7%, gold rose .24%, and silver rose 3.8% on the week in holiday thin markets. DIAMINDX is seasonally weak in November, but on average over the past 5 years, has bounced back in December (see graphic below for events that impact diamond sales). On the US jewelry front, holiday retailers are looking forward to a solid holiday sales season - likely lower than the blockbuster 2021 results but higher than 2019 - the "last normal year" the jewelry industry had - ie unimpacted by COVID. The US accounts for 51% of global diamond demand.

Both within and outside of the diamond industry there has been a focus on China, the world's second largest market for diamond demand with a 13% share. On Thursday, China reported a record number of daily Covid infections, which puts into question whether the country can ease lockdown restrictions and work toward ending its zero-tolerance covid policy. Protests have erupted in China due to the lockdowns, which weigh not only on diamond demand, but on global growth, and bring risk to supply chains. (See comment from Petra Diamond CEO Duffy in news section).

Graph: Key calendar events which impact diamond sales – seasonality in the diamond market (Source: Petra Diamonds)

Weakening in USD and the prospect of slowing Fed rate hikes, as discussed above, have helped support gold in recent weeks. Silver benefits from that as well, however, silver could be hampered by the prospect of a global growth slowdown given its industrial uses.

In an unusual move, Ghana is working on a plan to buy oil with gold instead of US dollars in an attempt to preserve its foreign currency reserves. Ghana is facing high inflation and a weak currency. Using gold would prevent the exchange rate from directly impacting fuel or utility prices. Ghana, a gold producing country, ordered its large scale mining companies to sell 20% of their refined gold to the central bank in preparation.

Chart: Though still in negative territory, Gold has just begun to outperform DIAMINDX for the year to date. Silver's return is approximately even with DIAMINDX. However, DIAMINDX is poised for a strong December due to seasonals.

Diamond News:

Christie's is holding a Magnificent Jewels auction in NYC on December 6th. It was set to auction a pink diamond weighing more than 13 carats. However, the diamond, which belongs to a private collector, has been withdrawn without explanation. Now, a 31.62-carat fancy blue diamond pendant necklace will lead the auction, with an estimate of $10m to $15m.

Petra Diamond announced the results of Tender 2 of FY 2023, at which 447,276 carats were sold for a total of US$61.3 million across Petra’s mining operations. "This is a creditable result in the current somewhat muted market, with like-for-like prices 12.6% higher compared to 2022 fiscal year tender two and 5.1% lower than tender one of fiscal year 2023,” says CEO Richard Duffy. Petra expects a supportive diamond market in the medium to longer term as a result of the structural supply deficit. Duffy noted, "There is the potential upside of festive season sales and any easing of lockdown restrictions in China.”

Ahead, DeBeers Sight 10 dates are December 5 - 9.

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.