Market Update Steady as She Goes

US equity indexes were mixed on the week: S&P500 -0.3%, NASDAQ -1.9%, and DJIA +0.6%. US economic data came in largely as expected, signaling a steady macro environment for now with with slowing inflation and growth. This was enough to keep US yields elevated. Equity indexes were a bit unnerved mid-week when Moody's downgraded 10 regional banks and put others on watch for downgrade. Market participants thought the timing of the downgrades was surprising - ie late - but not the information released as banks' balance sheets were closely examined by analysts post the SVB failure in March.

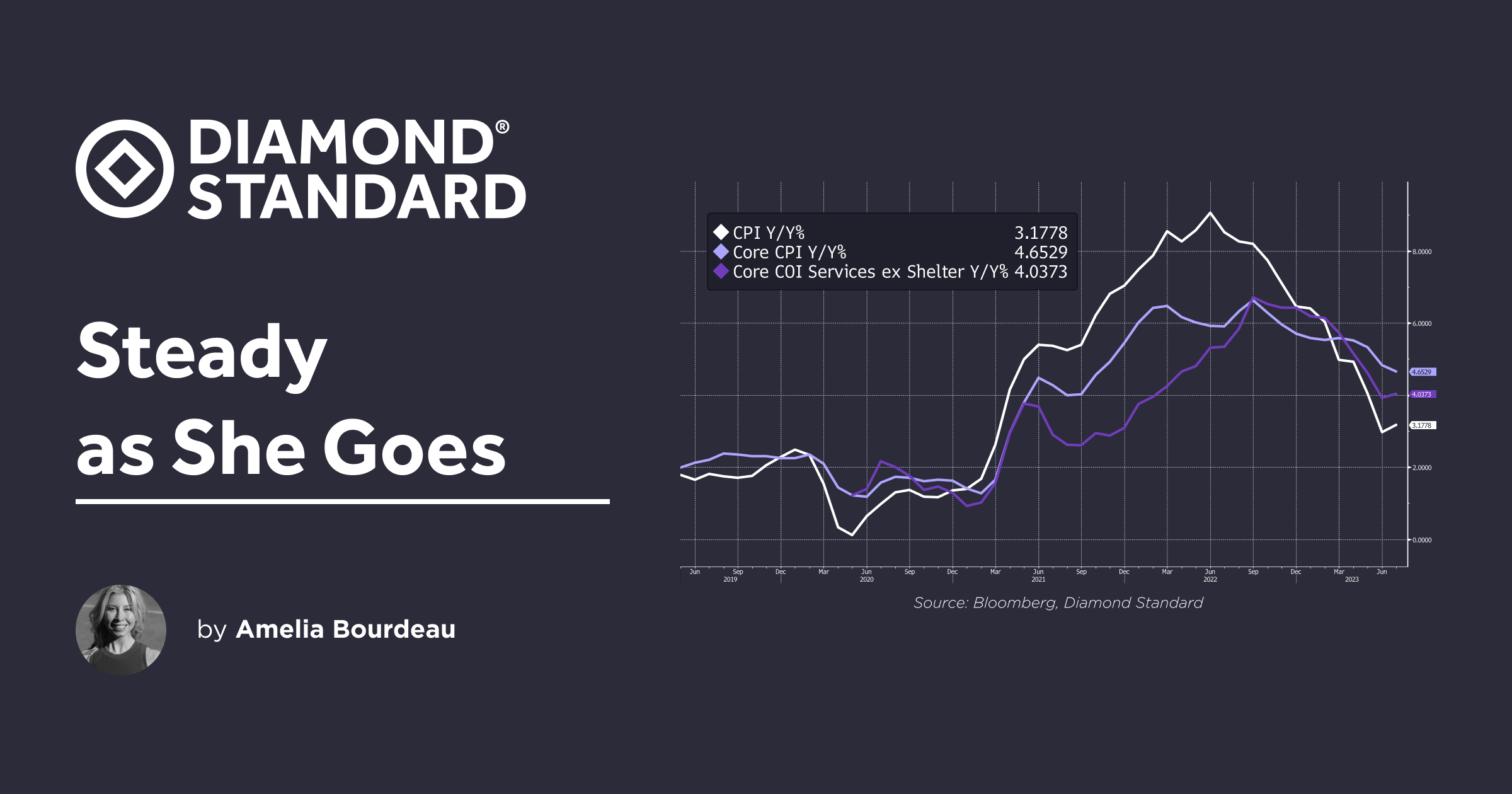

US economic data released this week were constructive. July CPI came in on expectations, rising 0.2% m/m for both the headline and the core readings. Headline CPI rose to 3.2% y/y from 3.0% previously. Core CPI ticked down to 4.7% y/y from 4.8% previously - its second consecutive read below 5.0%.

The latest initial jobless claims read was higher than expected at 248k vs 230k expected, indicating that the labor market continues to slow in an orderly way. The August preliminary read of the University of Michigan sentiment came in on expectations at 71.2. One year ahead inflation expectations ticked down from 3.4% to 3.3%. The 5-10 year inflation expectations also lowered to 2.9% from 3.0%. Both of these results are good news.

Market participants expect a pause at the September FOMC meeting. Fed fund futures are pricing in only a 11% probability of a 25bp rate at that meeting. The peak in the fed funds rate is priced as November at 5.41%. There are approximately 130bps of rate cuts priced in for 2024 as stronger growth in 2023 may cause sub-par growth in 2024.

Chart: US CPI, Core CPI, and Core CPI ex Services

Precious Metals:

Elevated US bond yields are weighing on gold and silver. Precious metals investors are waiting for a pivot in Fed language to more dovish and a signaling that rate cuts are ahead. For now, however, the dominant market narrative is for a US soft landing with the possibility of rates higher for longer. Absent a macro catalyst, gold could remain stuck in neutral for the time being.

A soft landing for the US economy and consumer would be positive for diamond prices as it would remove some uncertainty about the outlook. We focus on the US as diamond jewelry makes up 98% of the diamond market and the US is approximately 60% of global diamond market demand.

DIAMINDX was down 0.4% on the week to USD 4,690.

Lucara Diamond Corp. ("Lucara") released Q2 earning results. Lucara is a Canadian diamond mining company with a 100% owned producing mine in Botswana. According to Lucara, the mine, Karowe, "is one of world's foremost producers of large, high quality Type IIA diamonds in excess of 10.8 carats."

Q2 revenue came in at USD 41.1 million - down 21% y/y (Q2-2022). Profit came in at USD 5 million - down 60% y/y. Lucara noted that the change in quarterly revenue was driven by a softening of the market in H1 2023 compared to multi-year highs experienced in H1 2022, and a planned shift to lower-value diamonds at Karowe. On a like-for-like basis, prices "were soft". No changes were made to the company's guidance (released in December 2022).

In its earnings release, Lucara gave the following outlook on the diamond market, hitting key points:

"The longer-term outlook for natural diamond prices remains positive, anchored on improving fundamentals around supply and demand as many of the world’s largest mines reach their natural end of life over the next decade. Following on the record high diamond prices achieved in early 2022, a softer diamond market emerged in the latter half of 2022 which has persisted into the second quarter of 2023, the result of global economic concerns combined with geopolitical uncertainty, including the ongoing conflict in Ukraine. Prices continued to show signs of stabilization, however, as China continues to open-up post-Covid.

Sales of lab-grown diamonds increased during the period. Intense competition combined with improvements in technology continue to drive prices of lab grown diamonds down. This further differentiates this market segment from the natural diamond market and highlights the unique nature and inherent rarity of natural diamonds. The longer-term market fundamentals remain unchanged and positive, pointing to strong price growth over the next few years as demand is expected to outstrip future supply, which is now declining globally."

Gold and Silver

Gold fell 1.5% on the week to USD 1,913. USD 1,920 is resistance and 1,910 is support and USD 1,900 the larger support. Gold is being capped by a risk seeking environment with investors moving into equities. On a plus note, net central bank buying of gold returned to positive territory in June (the latest data). Central banks bought a net 55t of gold in June following three straight months of selling, according to the World Gold Council. Central bank buying has been providing a base for gold.

Silver fell 4.2% on the week to USD 22.65 - its fourth consecutive weekly loss. Silver broke downside USD 23.00 earlier in the week and remained in a narrow 23.00 - 22.60 range. The gold-to-silver ratio is at 84.40. 85.00 is a large resistance area.

Chart: Central Bank Buying/Selling of Gold (source: IMF IFS, WGC, central banks)

USD

USD (DXY Index) rose 0.8% to 102.85 at the time of writing - its fourth consecutive week of gains. The greenback is being supported by elevated US bond yields. USD is still sub 103.00, which is resistance and remains well within its larger range since the start of the year of 106.00 - 100.00. USD gained against all G10 currencies this week.

Chart: USD (DXY Ranges) and US 10 year yield

Sign Up for Market Commentary: Weekly insights on global markets and commodities from Diamond Standard by Amelia Bourdeau

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.