Market Update: Waiting for the Fed

US equity indexes were up on the week: S&P 500 +0.9%, NASDAQ +1.3%, and DJIA +0.9%. The S&P 500 rise was led by strong earnings from Meta, Microsoft, Alphabet, and Amazon. The VIX Index is subdued at a low of 15.78. The BoA MOVE Index, which measures implied volatility of one month treasury options, remains elevated at 122. On Friday afternoon, news outlets reported that the FDIC was preparing to place First Republic into receivership.

On the data front, the US Employment Cost Index increased a solid 1.2% in the first quarter, which translated to a 4.7% annualized pace. Wages & salaries and benefits for all workers each rose 1.2% over the quarter, suggesting compensation costs are not cooling just yet and most likely cementing a Fed rate hike next week.

Fed Pricing:

The FOMC decision is next week and Fed funds futures are pricing in an 80% chance of a 25bp rate hike. Market participants are less certain about the outcome of the June policy meeting - there is a 19% probability of another 25bp hike priced. 84bps of rate cuts are priced in from July through January 2024.

Precious Metals:

There were no large moves in precious metals or USD on the week as the market awaits next week's FOMC decision. Choppy trading conditions are likely into the announcement.

DIAMINDX was down 0.7% on the week to USD 5,210. Jewelry retailers remain cautious of a US consumer spending slowdown. On a positive note, US jobs gains have continued to be strong as well as wage data as seen this week for Q1.

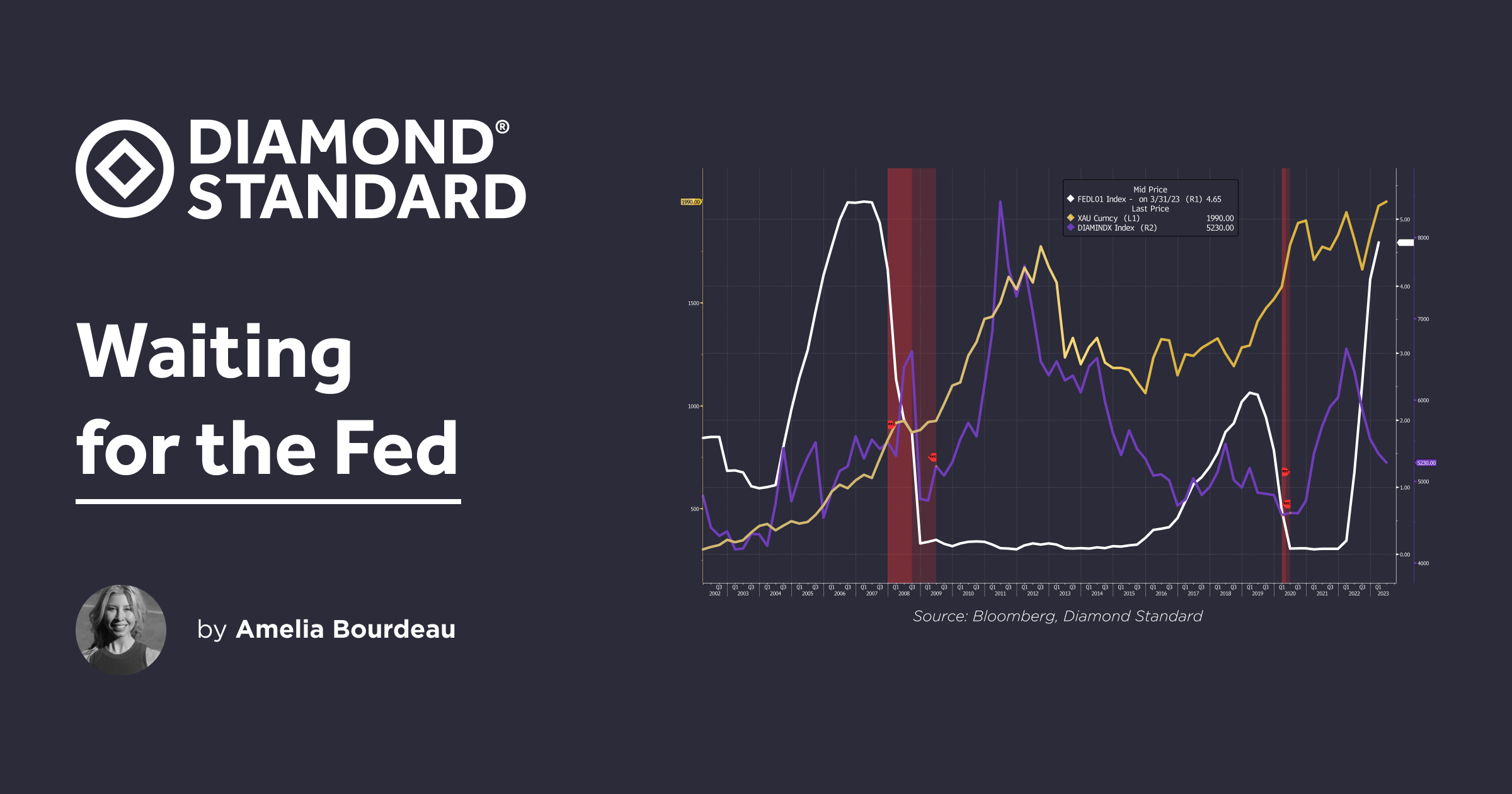

Market participants are pricing that we are nearing the Fed funds peak. The chart below looks at gold and DIAMINDX around the Fed funds peak for as long as data are available historically for DIAMINDX. This covers two US recession periods, which are shaded in red. During the Fed funds rate cuts, gold rallies while DIAMINDX falls. This is expected as diamonds, pre-financialization, are used for jewelry which is dependent on consumer demand which falls during a recession. Around the month after the recession ends, however, DIAMINDX begins to rally strongly.

Chart: Fed Funds Rate Peak, DIAMINDX, and Gold

In diamond industry news, DeBeers rough diamond production was flat on a year-on-year basis at 8.9 million carats in Q1 as the company transitions its Venetia deposit in South Africa to underground mining. DeBeers has maintained its production guidance for 2023 at 30-33 million carats.

Global luxury group Kering reported Q1 revenue. Total revenue was up 1% year-on-year. Kering’s "Other Houses", which includes jewelry was down 9% on a comparable basis. However, this was caused by a drop in wholesale revenue. On a positive note, the press release stated "Brioni’s sales were excellent, and the performance of Kering’s Jewelry Houses was outstanding."

Tiffany & Co, owned by LVMH, reopened its flagship NYC store on Fifth Avenue this week.

Gold and Silver

Gold rose 0.4% on the week to end at USD 1,990. Gold moved lower on Friday on the release of the US employment cost index, which supported another Fed rate hike.

Krishan Gopaul, strategist at World Gold Council ("WGC"), points out that "central bank [gold] demand of 1,136t in 2022 was the highest level of annual demand on record back to 1950." (see his chart here). It looks like central bank gold buying is continuing - this week, Gopaul noted that "the latest data from Monetary Authority Singapore shows their gold reserves increased by 17.3 tonnes in March. This means they have bought 68.7 tonnes of gold in Q1'23, lifting gold reserves to 222.4 tonnes (45% higher than at the end of December)."

WGC released its new Gold Market Primer: Market Size and Structure this week. WGC notes that the financial physical gold market, which is made up of bars, coins, gold ETFs, and central bank reserves, accounts for approximately 82,000t worth USD 5tn. That accounts for 39% of above ground stocks. In addition there is "a significantly smaller reported USD 1tn open interest in gold derivatives." Jewelry accounts for 95,547t worth USD 6tn (see chart below).

Chart: Value of above-ground gold and gold derivatives (from WGC)

*As of 31 December 2022. **Represents open interest in COMEX, TOCOM and OTC transactions. Source: Bloomberg, Bank for International Settlements, ETF company filings, ICE Benchmark Administration, Metals Focus, Refinitiv GFMS, World Gold Council

Silver was basically flat on the week, coming in at USD 25.05. That USD 25.00 area is one of consolidation, from which silver has had difficulty breaking upside. USD 24.00 is an area of support.

USD The USD (DXY Index) fell 0.2% on the week to end at 101.65. Since mid-April the DXY Index has been ranging 101.00 - 102.20.

JPY was the weakest G10 currency vs USD this week as new BoJ Governor Ueda asserted a more flexible BoJ policy stance, getting rid of the bank's forward guidance, and keeping its stimulus measure unchanged. This disappointed market participants who thought the BoJ would switch to a more hawkish stance. USDJPY broke resistance at 135.00 and ended the week at 136.30. JPY also reached multi-year lows vs EUR and CHF. GBP was the strongest G10 currency on the week gaining 1.1% vs USD as it is expected the the BoE will continue to raise its policy rate.

Chart: USDJPY vs US 10 yr yield. Despite the yield falling, USDJPY was higher - moving in opposite directions.

__Ahead next week: __

The main event is the FOMC decision and press conference on Wednesday. The Bloomberg consensus expects a 25bp rate hike. On Friday, US payrolls for April are released. The Bloomberg consensus expects a 180k gain.

Sign Up for Market Commentary: Weekly insights on global markets and commodities from Diamond Standard by Amelia Bourdeau

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.