Market Update: What the Fed Says

US equity indexes were down on the week: S&P500 -2.1%, NASDAQ -2.6%, and DJIA -2.2%. Equities were dampened by a US bond sell-off led by the longer-end of the curve on resilient economic data and a growing realization that, as a result, rates could stay higher for longer. July FOMC minutes added to this concern as the committee emphasized the need to bring inflation back down to its 2% target. The market is hyper-focused on what the Fed says. The US 10 year yield rose approximately 6 basis points on Thursday to 4.31%, just short of the October 2022 peak, which was the highest since 2007. Another factor weighing on equities - worries about global growth given the lackluster economic news out of China and its property market slowdown.

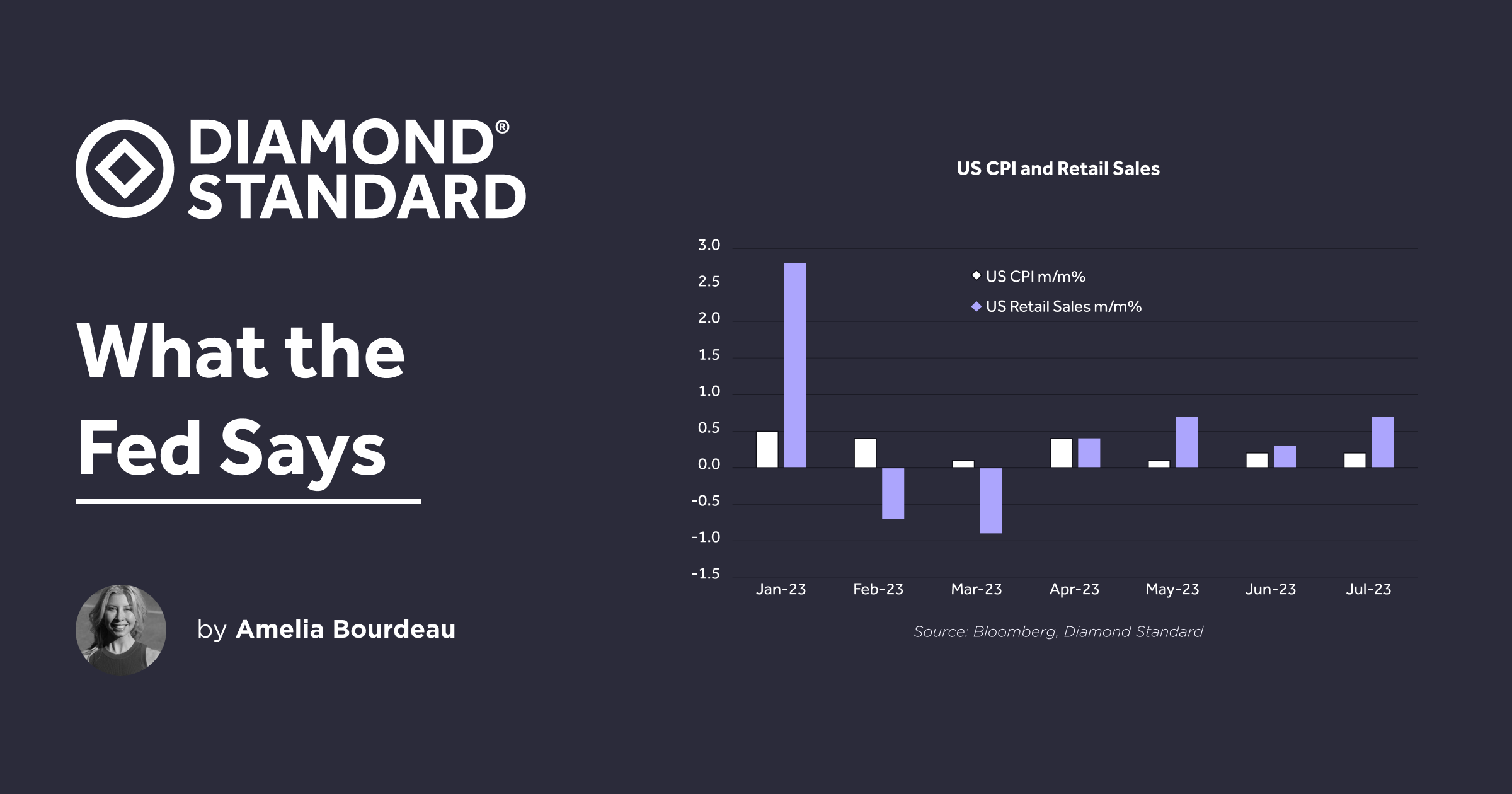

US economic data released this week showed the resilience of the US consumer. July retail sales surprised to the upside for all readings. Retail gains were fairly broad-based as nine out of 13 categories rose. Headline retail sales came in at 0.7% m/m vs expectations of 0.4% m/m. In addition, June saw an upward revision from 0.2% to 0.3% m/m. Retail sales ex autos and gas rose 1.0% in July vs expectations of 0.4% and also had an upward revision to June (0.3% to 0.4% m/m). The retail sales control group (the input to GDP for PCE) was double expectations at 1.0% m/m.

July FOMC Minutes noted that "the economy had been showing considerable momentum." The FOMC also stressed that "inflation remained unacceptably high" - seemingly intent on holding its benchmark rate higher for longer to ensure inflation is sustainably brought down toward its 2% objective.

Looking at FOMC policy rate pricing, market participants expect a pause at the September FOMC meeting. The focus has shifted to the length of time between the peak rate and the first fed rate cut. The peak in the fed funds rate is priced as November at 5.42%. There are approximately 120bps of rate cuts priced in for 2024 as stronger growth in 2023 may cause sub-par growth in 2024.

Ahead, the main economic event next week is Fed Chair Powell's speech at the annual Jackson Hole Economic Symposium on Friday, August 25th at 10:05am ET. This speech is both much anticipated and potentially market moving as market participants will be looking for signals on the policy rate path ahead.

Chart: US CPI and US Retail Sales m/m%. Inflation lower, retail sales robust.

Precious Metals:

Gold and silver remain under pressure from higher US bond yields and a strong USD. Precious metals investors are waiting for a dovish pivot in Fed language and a signaling that rate cuts are ahead - a move that would support precious metals prices. Currently, the dominant market narrative has shifted to a US soft landing in 2023 with the possibility of rates higher for longer. Absent a macro catalyst, gold could remain stuck in neutral for the time being.

A soft landing for the US economy and consumer would be positive for diamond prices as it would remove some uncertainty about the economic outlook, which both diamond mining companies and luxury goods houses have cited as the reason for caution currently (see below). We focus on the US as it is just over 50% of global diamond market demand.

However, with geopolitical risk, the timing of a US economic slowdown being fluid, and uncertainty on the path of the fed funds rate in 2024, an allocation to precious metals could benefit a portfolio through diversification.

DIAMINDX fell 0.2% on the week to USD 4,670. Here, we review some recent commentary on the natural diamond price decline and outlook from diamond mining companies and a luxury goods house:

Al Cook, CEO, De Beers Group in response to falling Cycle 6 rough diamond sales, cited seasonal trends as well as the diamond industry’s midstream sector taking a cautious approach to purchases in light of ongoing macroeconomic challenges.

Lucara Diamond Corp. ("Lucara") in response to falling revenue and profit for Q2 2023 noted that the change in quarterly revenue was driven by a softening of the diamond market in H1 2023 compared to multi-year highs in H1 2022. However, Lucara had a positive outlook for natural diamonds in the longer-term citing supply and demand dynamics: "The longer-term market fundamentals remain unchanged and positive, pointing to strong price growth over the next few years as demand is expected to outstrip future supply, which is now declining globally."

LMVH, the world's leading luxury products group, recorded H1 revenue up with the Watches and Jewelry category strong. Ahead, LVMH noted that it will rely on both the power of its brands and the momentum from the re-opening of the renovated Tiffany landmark store in NYC. Bernard Arnault, Chairman and CEO said, "Thanks to the desirability of our brands, we approach the second half of the year with confidence and optimism but will remain vigilant within the current environment and count on the agility and talent of our teams to further strengthen our global leadership position in luxury goods in 2023.”

H2 2023 is underway, so we look toward year-end: seasonally, the November - December months are supportive of diamond jewelry buying due to the US holiday season, merchant created shopping events such as "Black Friday" and "Cyber Monday", and in India, the Diwali wedding season.

Chart: DIAMINDX, US Retail Sales Y/Y%, US Payrolls Y/Y%.

Gold and Silver

Gold fell 1.2% on the week to USD 1,890. The yellow metal broke downside key level USD 1,900, hindered by the move up in the US 10 year yield and USD.

We have discussed previously that central bank buying has been providing a base for gold as institutional investment has been tepid. We look further at central bank buying below.

Last week, the World Gold Council, noted that net central bank buying of gold returned to positive territory in June after three months of net selling. This week, Metals Focus took a look at the drop in official sector gold purchases so far this year. In its latest Precious Metals Weekly report, Metals Focus says, "Net official sector purchases are estimated to have totaled 103t in Q2.23, marking the third consecutive quarterly drop and the lowest since Q1.22. This brought net buying to 387t for H1.23. While the total still marks the highest H1 figure in our data series (starting from 2013), it is down by 54% from the record high seen in H2.22."

They find that the pullback to date was largely driven by Turkey,"with the Central Bank of the Republic of Turkey (CBRT) selling 101t in H1.23. This marks a stark contrast to 2022 when the CBRT was the largest declared official buyer (+147t) globally." The majority of Turkey's selling happened from March-May due to local factors. Metals Focus notes that "a ban on gold bullion imports and surging gold demand, ahead of the parliamentary and presidential elections, resulted in a severe shortage of physical gold. Against this backdrop, the CBRT stepped into the market by providing extra physical gold liquidity in order to meet local demand." CBRT resumed gold buying in June.

Silver rose 0.1% to USD 22.71, remaining below USD 23.00 resistance. It continues to remain in a narrow 23.00 - 22.35 range. The gold-to-silver ratio is at 84.40. It broke topside the key 85.00 resistance area earlier this week just briefly - a level that bears watching.

Chart: USD (DXY Index), US 10 year yield, Gold (inverted), Silver (inverted). Higher US yields supporting the USD weighed on gold and silver.

USD

USD (DXY Index) rose 0.5% to 103.39 at the time of writing for its fifth consecutive weekly gain. USD broke topside 103.00 on the stronger than expected US retail sales and was further supported by the fed minutes. However, the DXY Index remains well within its larger range since the start of the year of 106.00 - 100.00. USD gained against all G10 currencies except the GBP this week. USDJPY broke topside 145.00, which is an area that Japanese authorities intervened last autumn.

Chart: USD (DXY Index) Ranges. This week, topside break 103.00.

Sign Up for Market Commentary: Weekly insights on global markets and commodities from Diamond Standard by Amelia Bourdeau

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.