Market Update: Yields Up

US equity indexes were down on the week: S&P500 -2.3%, NASDAQ -2.8%, and DJIA -1.1%. The market focus this week was rising US bond yields. The 10 year yield was up 12bps since last Friday, rising to 4.06% to end the week, but it did get as high as 4.17% on Thursday. The 30 year rose 21bps to 4.21%. These are levels not seen since early November 2022. It seems that the rally in US Treasuries weighed on US equity indexes. Furthermore, on Tuesday, in an unexpected move, Fitch downgraded the US's long-standing top credit rating of "AAA" down one notch to "AA+". The downgrade raises concerns that it could raise the federal government's borrowing costs.

US economic data and FOMC pricing:

US bond yields rose during the week on robust US economic indicators, which offered the first look at July data. Initial jobless claims were approximately steady on the week. ISM Services Index slowed but remained above the key 50 level.

July US payrolls came in a bit lower than expected at 187k vs expectations of 200k. The two month net revision was -49k. However, the unemployment rate fell to 3.5% from 3.6%. Average hourly earnings were higher than expected, coming in at 0.4% m/m and 4.4% y/y. These results show a gradual labor market moderation with rising wages, which should keep the hawks on the FOMC vigilant.

Fed pricing:

The peak in the fed funds rate is priced as November at 5.42%. Market pricing has converged to the Fed's forecast of no rate cuts this year. Fed fund futures are pricing in a 18% probability of a 25bp rate hike in September. There are approximately 120bps of rate cuts priced in for 2024.

Chart: US Payrolls - monthly and 3 month movg

Precious Metals:

Rising US bond yields weighed on gold and silver this week. Precious metals investors are waiting for a US recession scenario to cause Fed rate cuts, ie lower yields, supporting gold and silver. However, so far, the dominant market narrative is for a US soft landing with the possibility of rates higher for longer if core services inflation remains sticky. A soft landing for the US economy and consumer would likely be positive for diamond prices. Diamond jewelry makes up 98% of the diamond market and the US is approximately 60% of the global diamond market. Removing some uncertainty from the US consumer outlook would be a plus for the diamond market. However, markets and the fed remain data dependent and a US economic soft landing is not yet a given.

DIAMINDX fell 0.4% on the week to USD 4,720.

LMVH, the world's leading luxury products group, released H1 2023 results. It recorded H1 revenue of EUR 42.2 billion, which is up 15% from H1 2022 (organic growth, constant prices rose 17% from H1 2022). Revenue growth occurred across all groups except Wines and Spirits, which "faced a high basis for comparison."

Watches and Jewelry rose 11% from H1 2022 (+13% organic). LVMH noted that "Tiffany enjoyed excellent momentum with the exceptional success of the reopening of the 'Landmark' in New York; The Landmark has once again become an emblematic venue for New York life."

In a theme that is recurring among luxury goods companies, diamond miners, and diamond jewelry retailers, LMVH noted the uncertain "geopolitical and economic environment." Bernard Arnault, Chairman and CEO of LVMH, said in a press release, "Thanks to the desirability of our brands, we approach the second half of the year with confidence and optimism but will remain vigilant within the current environment and count on the agility and talent of our teams to further strengthen our global leadership position in luxury goods in 2023.”

Chart: LMVH and Richemont Equity Price vs DIAMINDX. DIAMINDX peaked later in the pandemic episode and continues to revert back to pre-pandemic levels, whereas the luxury goods houses' equity prices lowered and then had a resurgence starting in late 2022. The companies' luxury goods, of course, are more diversified than DIAMINDX and also targeted at wealthy consumers.

Gold and Silver

Gold fell 0.9% on the week to USD 1,941. Silver fell 3% on the week to USD 23.58. Gold and silver were impacted by movements in the rising rates in the back end of the US yield curve. Both recovered some on Friday with the weaker USD and some movement lower in US yields post the July payrolls result. The changing US economic outlook is creating volatility for longer-term US yields and therefore precious metals. The lack of participation from institutional investment is capping both metals.

Chart: US 10 year yield (purple), gold and silver (inverted), and USD (DXY Index, black). The move up in the 10year yield and USD weighed on gold and silver.

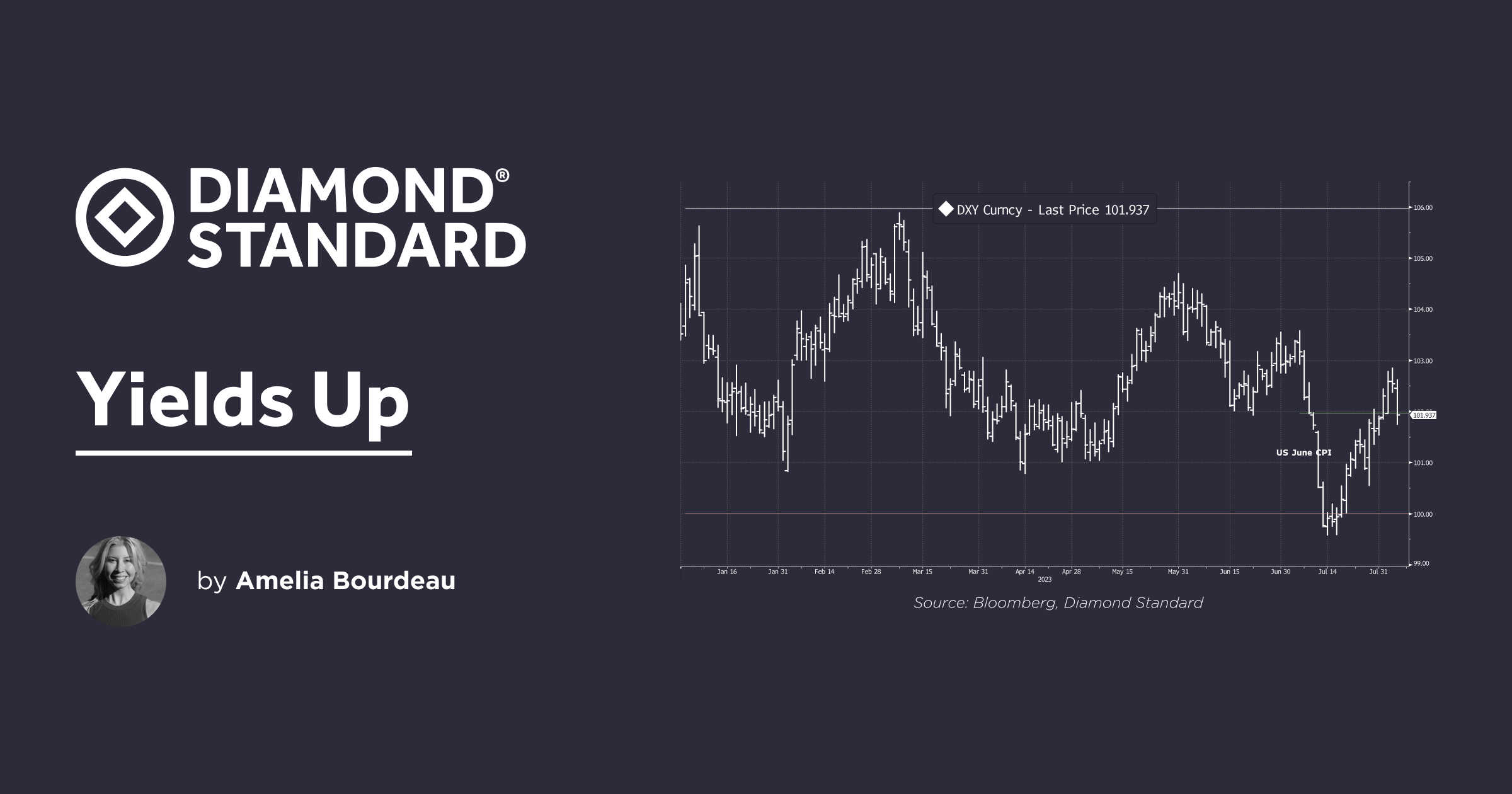

USD

The USD (DXY Index) rose 0.3% to USD 101.93 at the time of writing. The DXY did temporarily break 102.00 topside resistance this week. US payrolls coming in a bit under consensus weakened the USD on Friday as bond yields retreated some from the highs of the week. USD has been sub -102.00 since the release of the weaker than expected US June CPI on July 12th. The DXY Index also remains in its larger range of 106.00-100.00, which it has been in since the start of the year.

EURUSD was approximately flat on the week coming at 1.1014. The single currency has been trading just above and below the key 1.1000 level for a couple of weeks. GBPUSD fell 0.7% to 1.2753. The BoE hiked 25bps as expected to bring its policy rate to a 15 year high of 5.25%. The policy rate outcome, however, was split - two members voted for a 50bp hike, one voted for no hike, and the majority voted for a 25bps hike. BoE Chief Economist Pill warned that if food or natural gas prices surged again that the BoE would need to react. Worries about UK growth weighed on GBPUSD. JPY fell 0.5% to 141.86. The AUD was the weakest G10 currency vs USD this week, falling 1.2% to 0.6574. The RBA did not hike at its policy meeting - a dovish surprise as consensus expected more tightening.

Chart: USD (DXY Index) Ranges

Ahead next week:

US CPI for July and University of Michigan Sentiment - August Preliminary read are released. Philly Fed President Harker will speak on the economy.

Sign Up for Market Commentary: Weekly insights on global markets and commodities from Diamond Standard by Amelia Bourdeau

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.